Executive Summary:

| Standard | Content | Date |

| Decree N° 1270 | Decision No. 06/23 of the Common Market Council, which extends until 2038 the preferential origin regime of the Southern Common Market ("MERCOSUR") for Paraguay, is incorporated into the national legal system. | March 4, 2024 |

| Decree N° 1271 | Decision No. 05/23 of the Common Market Council, on the new Mercosur rules of origin, is incorporated into the national legal system. | March 4, 2024 |

| Decree N° 1398 | The agreement between Mercosur and Bolivia on the legal validity of certificates of origin and other related documents in digital format is incorporated into the national legal system. | March 19, 2024 |

| General Resolution NN° 02 | The administrative summary and reconsideration procedures for tax assessment and application of penalties were regulated. | February 16, 2024 |

| General Resolution N° 06 | A new regulation is established for the issuance of Electronic Tax Documents ("DTE") through the Ekuatia'i system. | March 26, 2024 |

| General Resolution N° 07 | The lack of confirmation of the voucher filing stub established in General Resolution No. 90/2021 is temporarily exempted from penalties, and the filing of the Financial Statements is extended. | March 27, 2024 |

More information:

► Decree No. 1270/2024 - Decision No. 06/23 of the Common Market Council, which extends until 2038 the Mercosur preferential regime of origin for Paraguay, is incorporated into the national legal system.

By means of Decree No. 1270/2024, the Executive Power incorporated into the national legal system the Decision of the Mercosur Common Market Council No. 06/23, "Mercosur Origin Regime", registered before the Latin American Integration Association (ALADI) as "Two Hundred and Nineteenth Additional Protocol to the Economic Complementation Agreement No. 18".

This provision extends until December 31, 2038, the differential origin treatment for Paraguay, according to which the tolerance of inputs from third countries for that State to issue the Mercosur certificate of origin is 60% of the FOB value of the goods produced or processed in Paraguay, which is fifteen to twenty percentage points (15-20pp) higher than the general tolerance of 40% and 45% for the other Mercosur States, which are determined as follows:

| MaxMNO (%) = VMNO / FOB x 100 |

MaxMNO: Maximum value of materials not originating in Mercosur, expressed as a percentage.

NAMV: Value of non-originating materials from Mercosur, which is the CIF value at import of the non-originating materials used in the production of the good.

FOB: Free on Board, which in this case refers to the FOB value of the exported product.

Paraguay was not the only beneficiary of this extension, as a similar regime was also extended until December 31, 2032, for Argentina and Uruguay, but in the case of Argentina, it only applies to its exports to Uruguay. These higher tolerances only apply to those items for which specific origin requirements are identified with an asterisk (*) in Appendix II of Mercosur Common Market Council Decision No. 05/23.

This decision will replace the previous extension contained in Mercosur Common Market Council Decision No. 13/21, once the new rules of origin, on which we will also comment on this occasion, also come into force. You can find more information on the previous extension incorporated into the Paraguayan legislation by means of Decree No. 8915/2023 by clicking here.

In this way, Paraguay retains its competitive advantage as an export development pole and a preferential access point to Mercosur for products from all over the world, which contributes significantly to the country's growth, especially through the maquila export regime.

► Decree No. 1271/2024 - Decision No. 05/23 of the Common Market Council, on the new Mercosur rules of origin, is incorporated into the national legal system.

By means of Decree No. 1271/2024, the Executive Power incorporated into the national legal system the Decision of the Mercosur Common Market Council No. 05/23, "Mercosur Origin Regime", registered before the Latin American Integration Association (ALADI) as "Ducentyeighteenth Additional Protocol to the Economic Complementation Agreement No. 18".

This provision updates and modernizes the Mercosur Regime of Origin ("ROM") to contribute to the facilitation of trade among the partners of the block, as well as its application for the competent authorities and commercial operators. It replaces the previous Decision No. 01/09 of the Common Market Council, incorporated into the national legal system by Decree No. 7057/2011.

According to the new ROM, products originating in Mercosur are (1) those wholly manufactured or obtained in its territory, (2) those manufactured in its territory exclusively from originating materials, and (3) those manufactured using materials not originating in Mercosur, but which have fulfilled the processing conditions sufficient to confer origin. Materials originating in Bolivia, Peru, the Andean Community and Colombia are also considered as originating in Mercosur, under certain conditions, by the agreements in force with those countries.

The products of the automotive sector, including assemblies and subassemblies, are governed, in terms of origin, by the provisions established in the respective bilateral agreements or, in their absence, by the domestic legislation, until the incorporation of the referred sector to Mercosur.

The specific requirements for a product to be granted Mercosur origin are those outlined in Appendix II of the above-mentioned regulations and may be: (a) change of tariff classification (change of tariff heading or subheading, as the case may be), (b) MaxMNO or (c) production process, as the case may be. If a product is subject to alternative origin criteria, it will be Mercosur originating if it meets one of them; while if it is subject to more than one criterion, it must meet all of them cumulatively.

Products resulting from operations or processes carried out in the Mercosur territory shall not be considered as originating when such operations or processes use exclusively non-originating materials and consist only of assembly or assembly, packaging, fractioning in lots or volumes, selection, classification, marking, the composition of assortments of products or simple dilutions in water or other substances that do not alter the characteristics of the product as originating, or other equivalent operations or processes or the combination of two or more of these processes.

The new ROM increases the general tolerance of MaxMNO for goods produced in the Mercosur States, which, with certain exceptions, increased by five percentage points (5pp), from 40% to 45% of the FOB value of the exported product. The MaxMNO is determined according to the formula expressed in the note on the higher margin of tolerance for Paraguay until 2038.

The new regulation also modifies the form of the certificates of origin, with the previous certificates being accepted during the 12 months following the entry into force of the new ROM. Apart from the new certificates, the exporting State Party may opt for a Declaration of Origin issued by the exporter or producer of the goods or use a combination of both.

This alternative constitutes a self-certification of origin, such as those already in operation in various preferential agreements entered by the United States or the European Union. Thus, a mixed regime is established that constitutes the so-called "proof of origin", which must be issued within 180 calendar days from the date of issuance of the commercial invoice (currently 60 days). The validity of the proof of origin is 12 months from the date of issue.

The new ROM will enter into force 30 days after the Mercosur Secretariat communicates to all States Parties the internalization of such rule in their respective legal systems, by Article 40 of the Ouro Preto Protocol, approved in Paraguay by Law No. 596/95. Since then, the previous Decision No. 01/09 of the Common Market Council, as well as Decree No. 7057/2011 which incorporated it into the national legal system, shall be abrogated.

► Decree No. 1398/2024 - The agreement between Mercosur and Bolivia on the legal validity of certificates of origin and other related documents in digital format is incorporated into the national legal system.

With the issuance of Decree No. 1398/2024, the Executive Power incorporated into the national legal system the Thirtieth Additional Protocol to the Economic Complementation Agreement No. 36 between the governments of the Mercosur member states and Bolivia ("Protocol"). By the Protocol, certificates of origin and other documents related to the certification of origin in digital format will have, between the signatory parties, the same legal validity and identical value as those issued on paper.

In order for such electronic documents to be valid, they must be issued and signed electronically, by the respective legislations of the signatory parties to the Protocol and comply with the procedures and technical specifications of the Digital Certification of Origin established in Resolution 386 of the ALADI Committee of Representatives.

The Protocol has an indefinite duration and will enter into force between Paraguay and Bolivia 30 days after both parties have notified the General Secretariat of ALADI of its incorporation into their respective domestic legislation. The same period will apply to Bolivia concerning the other Mercosur States individually.

► General Resolution No. 02/2024 - Administrative summary and reconsideration procedures for tax assessment and application of penalties were regulated.

The National Directorate of Tax Revenues ("DNIT") issued General Resolution No. 02/2024 ("RG-02"), whereby it updated the regulations of the administrative summary and reconsideration procedures for tax assessment and application of penalties, thus abrogating General Resolution No. 114/2017 as of Monday, March 1, 2024.

RG-02 clarifies that the subject of the summary proceedings and the appeal for reconsideration is the person subject to the summary proceedings and that this may be the taxpayer, responsible party or third party not involved in the tax obligation, including among them the legal representatives of the taxpayers, who, under certain conditions, have subsidiary liability for the taxes, as well as joint and several liability for the penalties of those they represent.

A novelty introduced by RG-02 is that the investigation must be carried out within a reasonable period of 4 months from the issuance of the resolution to initiate the investigation until the notification of the order to resolve, considering the complexity of the matter, the initiative shown by the defendants and the effects of the process on the defendant. This term may be extended, and its expiration does not entail the termination of the investigation or the dismissal of the defendant.

The deadlines for summary proceedings and appeals for reconsideration are computed in working days, from the day following the notification, being working days every day of the year, excluding Saturdays, Sundays, holidays, and national holidays, provided that the latter affect the entire working day. In this way, RG-02 summarizes and unifies the provisions on deadlines scattered in different regulations.

Another novelty introduced by RG-02 is that the appeal for reconsideration must be filed through the Marangatu System up to twenty-four hours (24:00 h) on the day of the expiration of the deadline set so that the extension up to 9 am of the following business day that was provided for in General Resolution No. 114/2017 is no longer admitted.

Now also, when the administrative act becomes final and the rectifying affidavits are not filed within the terms established in the particular resolution, in case they had been ordered, the DNIT may make the corresponding adjustments in the taxpayer's current tax account ex officio.

In the development of the procedure for tax assessment and application of penalties, the DNIT will gradually implement the tools of the electronic file, provided for in Law No. 6822/2021, such as the electronic seal, electronic signature and others; it will also indicate to the defendants the link through which they may access the records that gave rise to the Administrative Summary when they are available in the Marangatu System.

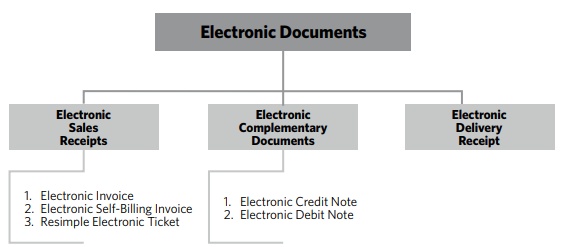

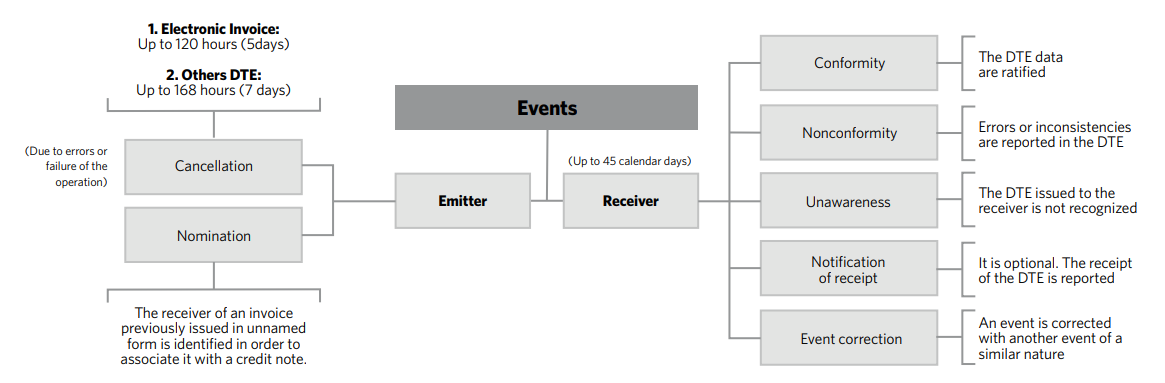

► General Resolution No. 06/2024 - The issuance of electronic tax documents through the Ekuatia'i system is regulated.

By means of General Resolution No. 06/2024, the DNIT established a new regulation for the issuance of DTE through the Ekuatia'i system, thus abrogating the previous regulation established by General Resolution No. 73/2020.

The main change brought about by this new regulation is the possibility that taxpayers who are individuals providing independent services may also issue DTEs. The referred resolution has designated a group of these taxpayers, who issue their invoices virtually through the Tesaká software, to obligatorily adhere to the Ekuatia'i system, thus abandoning the virtual issuance of vouchers.

In this regard, we have prepared an exclusive article for this regulation, in which we explain in more detail the scope and implications that this resolution will bring to taxpayers. You can access it by clicking here.

► General Resolution No. 07/2024 - Administrative measures are established for the confirmation of the annual and monthly stubs of RG 90; as well as extending the filing of financial statements for fiscal year 2023.

By means of General Resolution No. 07/2024 ("RG-07"), the DNIT provided that, until August 31, 2024, the lack of confirmation of the voucher registration voucher filing stub corresponding to:

- The annual registration of vouchers corresponding to fiscal years 2022 and 2023, under code No. 956 - REG. ANNUAL REG.

- The monthly register of vouchers corresponding to the fiscal periods from January to December 2023, and January and February 2024, under code No. 955- REG. MONTHLY VOUCHER REG.

This means that the lack of confirmation or late confirmation of the voucher registration voucher within the indicated period does not result in the application of a fine for contravention, nor the other negative consequences of non-compliance, such as: impossibility of generating the tax compliance certificate, increase of the taxpayer's risk index, among others.

It is worth mentioning that such measure is not new and has been reiterated since the electronic register of vouchers was established by means of RG-07. Examples of this are General Resolutions No. 124/2023, 126/2023 and 132/2023 of the former Undersecretariat of State for Taxation, as well as DNIT Resolutions No. 403/2023 and 730/2023, which had established this measure until April 30, 2024.

In addition to the above, RG-07 also establishes the extension of the deadline for the filing of the Financial Statements for the fiscal year ended December 31, 2023, of IRE taxpayers under the general regime. In this regard, taxpayers will have time until August of this year to file them, always remembering that the filings will be made according to the due date schedule established in General Resolution 38/2020.