A través de la Resolución MTESS N° 68/2024 (la “Resolución”) el Ministerio de Trabajo, Empleo y Seguridad Social (“MTESS”) establece los plazos de presentación de las planillas laborales para el periodo 2023, de conformidad a lo establecido en el artículo 10 de Decreto N° 8304 de fecha 27 de diciembre de 2017. La Resolución dispone que:

El plazo de presentación de las planillas laborales, en el periodo comprendido entre el 1 de marzo al 30 de abril de 2024.

Dispone que las planillas laborales contar con las siguientes especificaciones

SUJETOS: Empleadores del Registro Obrero Patronal con al menos un trabajador inscripto durante el Ejercicio Fiscal 2023.

CONTENIDO: la planilla de empleados y obreros debe contener: datos del trabajador: documento, nombre, apellido, sexo, estado civil, fecha nacimiento, nacionalidad, domicilio, cantidad de hijos menores, cargo, profesión, fecha de entrada, horario de trabajo, fecha de salida, motivo de salida; en caso de menores trabajadores: situación escolar, fecha del certificado otorgado por la CODENI; la planilla de sueldos y jornales debe prever: documento del trabajador, forma de pago, importe unitario, horas trabajadas de enero a diciembre, salario de enero a diciembre, horas extras acumuladas con recargo del 50%, salario acumulado por horas extras con recargo del 50%, horas extras acumuladas con recargo del 100%, salario acumulado por horas extras con recargo del 100%, aguinaldo, beneficios, bonificaciones, vacaciones, total de horas trabajadas en el año, total de salarios percibidos en el año, importe total por salarios, aguinaldo, beneficios, bonificaciones y vacaciones en el año; la planilla de resumen general de personas ocupadas debe contener: Cantidad de supervisores o jefes varones y/o mujeres, cantidad de empleados varones y/o mujeres, cantidad de obreros hombres y/o mujeres, cantidad de menores varones y/o mujeres.

DECLARACION JURADA: luego de la presentación no pueden ser modificadas las planillas dado que tiene carácter de declaración jurada.

Este contenido tiene únicamente fines informativos generales y no debe ser considerado como asesoría legal puntual. Si precisa asesoramiento específico no dude en contactarnos.

Risk assessment agency Standard & Poor's has announced its decision to raise the country's credit rating to BB+ with a Stable outlook. This upgrade comes a decade after the previous rating increase to BB (Stable) in 2014.

The credit rating boost is attributed to the observed increased economic resilience of the country. In this regard, the agency anticipates that sustained economic growth could alleviate spending pressures and potential climate-related risks in the country, while also contributing to the national government's ability to stabilize debt.

The rating agency expects that macroeconomic stability and an excess supply of renewable energy will attract investments, supporting growth and contributing to a gradual diversification of the economy.

Economy Minister Carlos Fernández Valdovinos commented on the matter, stating that this achievement will create more opportunities for investments and economic growth, instill greater confidence in investors, and enable the country to access improved financial conditions.

We are pleased to announce that we have advised Marriott International on various aspects related to the operation and management of the country's first “five-star plus” luxury hotel. This exclusive establishment will carry the prestigious “JW Marriott” brand and will be constructed by Agri Terra in the heart of Asunción, the capital of Paraguay.

As legal representatives of Marriott International, Vouga Abogados played a pivotal role in conducting comprehensive due diligence reviews in corporate and real estate matters. The transaction involves the construction of an innovative mixed-use building in the burgeoning financial and business district of Asunción. Designed by the architecture firm DPA Designs, led by Daniel and Sebastián Piana based in Buenos Aires and Miami, this development will house the JW Marriott hotel, along with commercial, corporate, and residential units. Furthermore, it represents a significant investment in Paraguay's real estate and hotel sectors. Construction is expected to commence in 2024, generating employment for over 3,000 workers and contributing to the evolution of Asunción's growing urban skyline. DPA Designs' architectural vision promises to make the building an iconic landmark in the city's dynamic profile.

Marriott International, headquartered in Maryland, USA, holds the title of the world's largest hotel chain, operating in over 130 countries with more than 8,000 properties under its 31 renowned brands, including Ritz-Carlton, St. Regis, Sheraton, Westin, and Le Meridien. With annual sales exceeding $20 billion, Marriott International continues to be a global leader in the hotel industry.

Vendrell & Herrera led the drafting and negotiation of transaction documents on behalf of Marriott International.

We are excited to have been part of this unique collaboration that will contribute to the economic and architectural development of Paraguay. We remain committed to excellence and innovation in every project we undertake.

El pasado martes 23 de enero de 2024, la Comisión de Ciencia, Tecnología, Innovación y Futuro de la Cámara de Senadores (“Comisión”) convocó a una Mesa de Trabajo para analizar el proyecto de ley de Protección de Datos Personales en Paraguay en la Cámara de Diputados el pasado 5 de mayo de 2021 (“Proyecto de Ley”). Si bien el Proyecto de Ley aún se encuentra en su primer trámite constitucional, el mismo ya cuenta con dictámenes de las comisiones de Relaciones Exteriores, Ciencia y Tecnología e Industria y Comercio de la Cámara de Diputados y ya fue incluido en el orden del día de la sesión del 6 de diciembre de 2023 aunque no fue tratado. En ese sentido, entendemos que la convocatoria de la Mesa de Trabajo para tratar el Proyecto de Ley en la Comisión es un indicio de que el Proyecto de Ley podría retomar su trámite a la brevedad y que debería haber novedades durante el primer semestre de este año.

El Proyecto de Ley tiene por objeto la protección de los datos personales de las personas físicas para garantizar el ejercicio pleno de estos derechos, así como su la libre circulación. Por otra parte, el Proyecto de Ley aplica al tratamiento, total y parcial, automatizado o no, de los datos personales por parte de terceros, sean estas personas físicas o jurídicas. En ese sentido, es importante señalar que uno de los efectos principales de la promulgación del Proyecto de Ley sería la necesidad de adecuación de las políticas de privacidad, de cookies y los términos y condiciones de uso de todas las páginas web y plataformas de comercio electrónico que recojan y traten datos de terceros. Asimismo, una vez promulgado, el Proyecto de Ley podría derogar, al menos parcialmente, la Ley 6534/2020 de “Protección de Datos Personales Crediticios”; norma que actualmente rige en Paraguay como ley de protección de datos personales con carácter general.

The real estate tax values for the taxable base of the real estate tax and its additions, corresponding to fiscal year 2024, are established.

December 28, 2023

Decree N° 872

The issuance of electronic receipts through the Integrated National Electronic Invoicing System ("SIFEN") is regulated.

December 18, 2023

Decreee N° 859

Expands the customs declaration requirements in detail and the selectivity channels subject to controls after the customs operation.

December 18, 2023

General Resolution No. 730/2023

The National Directorate of Tax Revenues ("DNIT") exempts from penalties until April 30, 2024, the lack of confirmation of the receipt filing annual and monthly, established in General Resolution No. 90/2021.

December 29, 2023

Latin American Tax Policy Guide

VOUGA Abogados has contributed to the drafting of the latest tax guide of the World Services Group ("WSG").

December 22, 2023

More information

► Decree No. 947/2023 - Whereby the real estate tax values are set for the taxable base of the real estate tax and its additions, corresponding to fiscal year 2024.

By means of Decree No. 947/2023, the Executive Branch fixed the real estate tax values established by the National Cadastre Service ("SNC") of the Ministry of Economy and Finance, which will serve as the taxable base for determining the real estate tax and its additions for the fiscal year 2024.

The adjustment involves a 3.5% increase in real estate values for urban and rural properties based on the year-on-year variation of the Consumer Price Index ("CPI") at the end of October 2023, as issued by the Central Bank of Paraguay.

It is important to remember that the amount of the tax is determined by applying the corresponding rates (usually 1%) on the tax valuation of the real estate established by the SNC (taxable base), which is made up as follows:

Urban real estate: Land value (m2 of the property per G/m2) plus building value (m2 of the buildings per G/m2). The G/m2 are determined by the type of pavement with the highest value of the property's adjoining streets (fronts) for the land value, and by the construction category for the buildings.

Rural properties: Land value (hectare ("ha") of the property per G/ha). The tax valuation of each district is determined according to its opportunity cost (distances to urban centers and accessibility) and the predominant type of soil, according to the categories indicated in the decree.

It also provides, among other things, the valuation of properties that change from urban to rural category and vice versa, the procedure for the exemption of 50% of the tax for rural properties with forestry priority or with real right of forestry surface, and the discount for rural properties with low productive areas that differ from the type of soil of their district.

The amount of the tax to be paid to the municipality can be consulted through the SNC website, in the municipalities section, real estate tax liquidation section, subsequently selecting the department of residence, the district and the cadastral nomenclature of the property (cadastral register or current account).

Decree No. 872/2023 - Whereby the issuance of electronic receipts through SIFEN is regulated.

By means of Decree No. 872/2023 (the "Decree"), the Executive Branch regulated the issuance of sales receipts and other electronic tax documents through SIFEN from January 1, 2024, onwards. Thus, Decree No. 7,795/2017, by which the SIFEN was created, was abrogated since then.

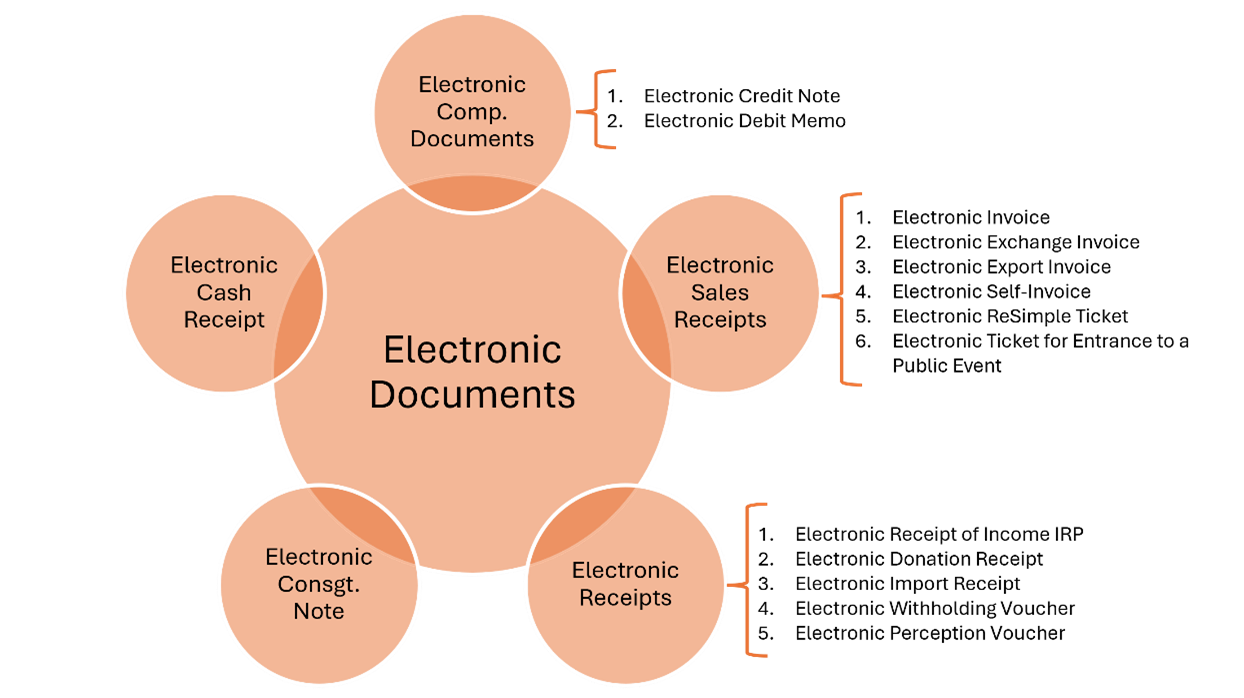

The Decree addresses the issues related to the electronic invoicing: (1) types ofelectronic documents, (2) processes related to them (generation, delivery, consultation, and conservation), (3) acts or events on such documents, depending on who performs them (issuer, receiver, SIFEN and DNIT), and (4) conditions to be an electronic invoicer. Regarding the classification of electronic documents, the Decree establishes the following groups, without prejudice that the DNIT may incorporate others:

The Decree includes several concepts already defined in General Resolution No. 23/2019 of the former SET and regulates aspects that were not fully clarified in the previous regulations governing electronic invoicing. Below, we mention some of the most relevant issues the Decree addresses.

Commercial transactions carried out by an issuer who is a natural or legal person are classified according to the concept invoiced and the quality of the recipient of the electronic document: (a) B2B if it is a taxpayer that does not act as the final consumer, (b) B2C if it is a natural person that acts as the final consumer, (c) B2E if it is a foreign person to whom goods are exported, (d) B2F if it is a foreign person that receives a service (the classification for the sale of goods abroad would remain in doubt), and (e) B2G if it is a public entity of Paraguay.

In none of these types of transactions is it allowed to issue an electronic invoice in unnamed form, i.e., in which the recipient is not identified except for B2C transactions that do not exceed the following amounts or their equivalent in foreign currency: (i) G. 35,000,000 as from January 1, 2024, and (ii) G. 7,000,000 as from January 1, 2025. This constitutes a reduction of the limit for issuing unnominated invoices in B2C transactions, since General Resolution No. 23/2019 had set it at USD 10,000 or its equivalent in guaraníes, except for deliveries of medical samples by importers or national laboratories, which were not subject to this limit.

The Decree also establishes requirements regarding electronic export invoices, which the exporting entity must issue before the formalization of the dispatch and departure of the goods from Paraguayan territory. The invoices will be used to support the cancellation of the definitive export affidavit.

An important figure introduced by the Decree is the electronic exchange invoice, which is defined as the electronic document generated as a credit title issued to an order payable by the purchaser of a good or service. Although the figure of the exchange invoice was already established through Law No. 6,542/2020, the Decree incorporates this figure (basically an invoice issued on credit) within the SIFEN, thus seeking to make it operative through this system.

It is also worth mentioning the creation of the electronic receipts of money, which document the payment in credit or term operations, as well as income of money for which there is no obligation to issue an invoice or other tax document. In credit or term operations, the receipt must be associated with the electronic invoice that supports it. The money receipt may not be used to support Value Added Tax ("VAT") credit, but it may be used to support income tax-related expenses, depending on the rules applicable to each tax.

Regarding the processes and events related to electronic documents, the Decree does not introduce substantial changes concerning what was provided for in General Resolution No. 23/2019 of the former SET. However, the introduction of new events can be observed, such as the nomination by the issuer (the recipient of an unnamed document is identified after issuance), the consent of the recipient for Electronic Credit Notes and the challenge of documents by the DNIT, also foreseeing the power of the latter to create new events for the SIFEN.

Finally, the Decree established the conditions that apply to those taxpayers who wish to register as electronic billers, which are: (i) acquire the qualified electronic signature certificate; (ii) possess a computerized billing system that allows the issuance, receipt and storage of electronic tax documents and their associated events; (iii) request authorization and stamping for electronic documents; (iv) request and obtain SIFEN authorization as an electronic biller; and (v) obtain the taxpayer's security code for the generation of the QR to be incorporated in the graphic representations of the electronic tax documents.

The DNIT is also empowered to designate taxpayers as electronic billers gradually, without prejudice that the interested parties may voluntarily become electronic billers. They will not be able to issue receipts or other tax documents by means other than electronic means from the date indicated by the DNIT, except in contingency cases.

► Decree No. 859/2023 - Whereby the customs declaration requirements in detail and the selectivity channels subject to controls after the customs operation are expanded.

By means of Decree No. 859/2023 (the "Customs Decree"), the Executive Branch amended Articles 170 and 331 of the Annex to Decree No. 4672/2005, which regulates the Customs Code, which deals with (1) the requirements of the customs declaration in detail and (2) the subsequent controls of the customs duty, respectively. This provision also abrogated Decree No. 2908/2019, which amended Article 331.

Regarding the customs declaration in detail, the Customs Decree expanded the information it must contain. Hence, it now also includes data relating to the persons responsible for and intermediaries of the freight. The obligation to attach the following documents to the customs declaration in detail was also added:

Invoice or receipt for license or brokerage payments and other expenses related to the goods, which are part of the customs value of the goods, and which are not included in your invoice.

Invoice or freight receipt issued by a national or foreign company with legal representation and legal status in the national territory, specifying the expenses and costs incurred.

Invoice or proof of expenses and costs for handling, brokerage and other payments that are part of the customs value of the goods and that are not included in the invoice of the goods or freight.

Proof of payment specifying the means and form of payment for the goods, by the legal regulations of the Secretariat for the Prevention of Money or Asset Laundering ("SEPRELAD").

It is important to remember that the detailed declaration must be filed even when the declared goods are affected by customs regimes or treatments not subject to the application of taxes or economic restrictions on imports or exports, whether exempt or exempted from them unless otherwise specified.

About subsequent controls of goods, the Customs Decree expands the selectivity channels whose goods are subject to them, as it provides that all selection channels are subject to such controls, including the red channel and no longer only the green and orange channels, as previously provided for.

Subsequent controls are performed after the release of the goods and are carried out at two (2) levels: (i) a first level of review of the declarations to verify the tariff classification, origin, valuation, and tax liquidation of the goods; and (ii) a second level of control of documents in the company itself, which includes computer systems, accounting records and warehouses linked to customs operations.

► Resolution No. 730/2023 - DNIT exempts from penalties until April 30, 2024, the lack of confirmation of the presentation of the receipt registry, established in General Resolution No. 90/2021.

By means of Resolution No. 730/2023 ("R-730"), the DNIT provided that, until April 30, 2024, it will not consider as tax non-compliance the failure to confirm the filing of the registration of receipts corresponding to:

The annual registration of vouchers corresponding to fiscal years 2022 and 2023, under code No. 956 - REG. ANNUAL REG.

The monthly register of vouchers corresponding to the fiscal periods from January to December 2023, and January and February 2024, under code No. 955- REG. MONTHLY VOUCHER REG.

This means that the lack of confirmation or late confirmation of the voucher registration voucher within the indicated period does not result in the application of a fine for contravention, nor the other negative consequences of non-compliance, such as: impossibility of generating the tax compliance certificate, increase of the taxpayer's risk index, among others.

This measure complements the provisions of the former SET in General Resolutions No. 124/2023, 126/2023 and 132/2023, as well as those of the DNIT in Resolution DNIT No. 403/2023, which had established this measure until December 31, 2023.

During the R-730's validity period, the DNIT will continue to receive the receipt registration and confirmation of the filing slip.

► Guide to tax policies in Latin America - VOUGA Abogados has contributed in the drafting of the latest WSG tax guide.

The WSG Tax Group has published its latest tax guide, "Navigating Tax Law Policies in Latin America”, which provides detailed country-by-country perspectives, updates, and trends regarding tax laws and policies in the region.

More than 35 tax experts from 17 Latin American jurisdictions contributed to the guide, a testament to the power of partnerships among WSG members and their highest expertise on crucial industry updates and trends.

In that sense, VOUGA Abogados has contributed to the guide with a chapter on Paraguay and its tax policies by our distinguished members, Rodolfo Vouga, Horacio Sanchez and Andrés Vera.

It is worth mentioning that the WSG is the foremost global network of independent law firms, providing a unique environment and platform to connect its members with the most elite law firms and their multinational clients worldwide. If you wish to consult the complete guide, you can do so through the following link.

Enactment of Law 7237/2023 "Establishing special provisions and financing for the execution and implementation of the suburban train between the city of Asunción and Ypacaraí, under the responsibility of the Ministry of Public Works and the Paraguayan Railways Company S.A.; and authorizing the respective subcontracting agreement."

December 26, 2023

Call for Bids

The National Directorate of Public Procurement (“DNCP”) has published on its portal the invitation to an International Public Tender (“IPT”) for the National Route No. 17 Improvement Project, connecting Pedro Juan Caballero – Capitán Bado – Itanará – Ypejhú in the Departments of Amambay and Canindeyú.

January 5, 2024

Resolution

The Ministry of Public Works and Communications (“MOPC”) issued Resolution No. 2218 announcing the five prequalified consortia that will continue participating in the bidding process 1288 "Call DIPE 01/2023 Prequalification Public Investment Project for the Expansion and Improvement of Route PY01, in the section between Cuatro Mojones and Quiindy."

December 29, 2023

Law

Update on the status of the water and sanitation project for the Metropolitan Area of Ciudad del Este, financed by the Inter-American Development Bank (“IDB”) and the Japan International Cooperation Agency (“JICA”) for a total of USD 200,000,000.

May 11, 2023

Law

Update on the water and sanitation project for the Metropolitan Area of Asunción – Lambaré Basin, financed by the Inter-American Development Bank (“IDB”) and the Official Credit Institute of the Kingdom of Spain (“ICO”) for a total of USD 165,000,000.

April 24, 2023

Law

Enactment of Law 7182/2023 approving the loan agreement between the Republic of Paraguay and the Andean Development Corporation (“CAF”) for an amount of USD 160,000,000 for the financing of the water and sanitation project for the Metropolitan Area of Mariano Roque Alonso.

October 18, 2023

More Information:

► The Executive Branch enacted Law 7237/2023, which establishes the financing conditions for the execution and implementation of the "Suburban Train" Project.

General Aspects

On December 26, 2023, the Executive Branch enacted Law 7237/2023 (the "Law"), which provides special provisions and financing for the execution and implementation of the suburban train project, powered by renewable energy. The route will stretch between the cities of Asunción and Ypacaraí (the "Project").

The MOPC and the Paraguayan Railways Company S.A. (“FEPASA”) will be responsible for executing the Project.

Project Financing

The Law authorizes the Ministry of Economy and Finance (“MEF”) to undertake the necessary steps for Project financing. In this regard, the Law specifies that, for the credit instrument to be valid, it must receive approval from Congress. Furthermore, the MEF will assume financial commitments only after the approval of the loan agreement, which must adhere to the terms of the Law.

Establishment of Guarantee and Liquidity Trust

The Law anticipates the creation of a guarantee and liquidity trust, where the MEF will be the settlor, and the Financial Development Agency (“AFD”) will act as the trustee.

The purpose of the trust is to manage all resources generated by the Project, including those used to finance availability payments outlined in the Law. Payments will be unconditional and irrevocable. The Executive Branch will regulate the guidelines and regulatory mechanisms of the trust and availability payments; as of now, this regulation has not been promulgated.

Implementation Agreement

It is important to note that the Project is structured as a government-to-government agreement between the Republic of Paraguay and the Republic of Korea (South). The Law empowers the MOPC to sign an implementation agreement with the Korean Public Organization, Korea Overseas Infrastructure & Urban Development Corporation (KIND)[1], outlining the commitments of the parties within the Project framework.

While the Project will be governed by the Law and not by Law No. 5102/2013 "PROMOTION OF INVESTMENT IN PUBLIC INFRASTRUCTURE AND EXPANSION AND IMPROVEMENT OF GOODS AND SERVICES PROVIDED BY THE STATE" (the “PPP Law”), the final structure of the Law, once regulated, is likely to be similar to that of the PPP Law.

It is noteworthy that Article 11 of the Law states that, within the Project's development, KIND may avail itself of the benefits of Law No. 60/1990 "APPROVING, WITH AMENDMENTS, DECREE-LAW NO. 27, DATED MARCH 31, 1990, 'AMENDING AND EXPANDING DECREE-LAW NO. 19, DATED APRIL 28, 1989,' 'ESTABLISHING THE FISCAL INCENTIVE REGIME FOR INVESTMENTS OF NATIONAL AND FOREIGN ORIGIN CAPITAL.'"

Project Payment Mechanisms

The MEF will provide the concessionaire or sub-concessionaire with availability payments in U.S. dollars through the trust ("Payments"). However, Payments will be made only once the quality, service, and performance indicators set by the MOPC and FEPASA are met. They are the ones authorized to instruct payment to the MEF when applicable.

Payments will become unconditional and irrevocable once the compliance with quality and service indicators is approved.

Land Release for Project Execution

The MOPC and FEPASA will be responsible for: (i) land release, (ii) land acquisition, (iii) relocation, (iv) compensation, (v) cleaning of the areas involved in the Project execution, and even (vi) release of necessary dominion strips under the expropriation regime provided for in Law No. 6084/2018.

This is likely to be one of the most challenging aspects of Project realization since successful negotiation with neighbors whose properties currently occupy the dominion strip and oppose the Project with the current layout will be necessary.

Project Value, Timelines, and Scope

The Project is valued at approximately USD 550,000,000, and its construction is estimated to take around 4 years, with a sub-concession period of 30 years. In this regard, Article 5 of the Law establishes that the sub-concession contract will be granted to KIND by the Executive Branch through FEPASA (the "Contract"). Likewise, once the Contract is signed, KIND will be obligated to secure financial closure to finance the Project, in accordance with the terms established in the Contract and regulations.

The Project will cover a distance of 43 kilometers, connecting Asunción with the towns of Luque, Yukyry, Areguá, Patiño, and Ypacaraí. The route traverses one of the country's most densely populated areas; therefore, it is expected that the Project's realization and operation will significantly reduce inbound and outbound traffic to the capital, in addition to considerably improving public transportation conditions for citizens.

► International Public Tender call for surveying, compensation, expansion, and improvement of Route PY 17 “Route of Sovereignty”

General Aspects

On January 5, 2024, the National Directorate of Public Procurement (DNCP) published on its portal the call for Tender 438107 convened under the IPT procedure for the survey, compensation, construction, and maintenance of the pavement of Route PY 17. This route connects the towns of Pedro Juan Caballero – Zanja Pyta – Capitán Bado – Itanará – Ypejhú, in the departments of Amambay and Canindeyú (the "Project").

The Project aims to improve the connection between two of the country's most important productive areas. It is estimated that it will benefit approximately 150,000 people.

The execution of the Project includes, among others, works such as: earthworks, drainage; construction of the structural package, main axis, and accesses; paving; complementary works such as construction and removal of fences, signage, lighting, weighing and toll booths, counting booths, and environmental management plan.

Investment Amount

₲1,432,191,265,000 (Approximately USD 215,000,000). The Project will be financed with a loan from the Financial Fund for the Development of the La Plata Basin (“FONPLATA”).

Offer Maintenance Guarantee

3% - insurance or bank guarantee.

Deadline for Submission of Bids

Friday, January 26, 2024. (9:00 a.m.)

Adjudication System

Per lot. The Project is divided into 4 lots. The adjudication of more than one lot to an offeror is allowed. Below is the planned length for each lot.

Lot 1 – 44 km

Lot 2 – 48 km

Lot 3 – 53 km

Lot 4 – 48,3 km

Each lot includes all aspects of the Project, i.e., surveying, compensation, construction, and maintenance of the work. The value of each lot is:

Lot 1 – Gs. 377.025.115.000

Lot 2 – Gs. 344.584.917.000

Lot 3 – Gs. 386.590.367.000

Lot 4 – Gs. 323.990.866.000

Approximately USD 53,000,000 on average, depending on the exchange rate.

Award Criteria

The contracting party will award to the bidder that substantially complies with the requirements and offers the lowest evaluated price. This is subject to the bidder being considered eligible according to the criteria specified in the bidding terms and conditions.

Advance Payment

The tender envisages granting a 15% advance to the awarded bidders.

Term for execution of works

24 months from the start order.

Maintenance Period for Service Levels (KPI)

60 months after the completion of the works.

Contracting Systems

Construction works: unit prices

Execution of surveying and expropriations for lands and improvements: provisional sums

Maintenance for service levels: lump sum

Bid validity period

150 calendar days counted from the deadline for bid submission.

Offer maintenance guarantee validity period

180 days counted from the submission of bids.

Bid Submission

National or foreign companies, individually or in consortia, with legal, economic-financial, and technical capacity.

Subcontracting

Subcontracting for the execution of some planned works is allowed, but the amount of subcontracted work cannot exceed 40% of the total contract amount. However, the awarded company must obtain prior authorization from the contracting entity.

► Awarding for the Design of the Expansion and Improvement Project of the “Silvio Pettirossi” International Airport

General Aspects

In late October 2023, the National Directorate of Civil Aviation (“DINAC”) announced that the architectural firm BMA, Carlos Ott, and Carlos Ponce de León were awarded the design of the new “Silvio Pettirossi” International Airport, as a result of the international selection process carried out for the project. Once the design is analyzed, the Executive Branch will issue the call for the construction and operation tender for the airport (the "Project").

Investment Amount and Project Dimensions

The Project's implementation will cost approximately USD 242,000,000. The dimensions of the works are estimated to be between 40,000 m2 and 78,000 m2. It is expected that the Project will double the terminal's capacity movement within a period of 10 years.

Contracting Authority

The MOPC.

Financing

The financing modality is not yet defined; however, it is most likely to be under the Public-Private Partnership (PPP) modality. The construction of the Project is estimated to take approximately 3 years, and if a concession is chosen, the contract could extend for up to 30 years.

► Prequalification for the Expansion and Improvement Project of Route PY 01, Cuatro Mojones - Quiindy Section

General Aspects

Early last year, the DNCP published Tender 1288convened by the MOPC for prequalification for the expansion and maintenance project of Route PY 01 (the "Tender"). The Tender aims to form the list of prequalified bidders for the awarding of a Public-Private Partnership (PPP) contract governed by Law 5102/2013 ("PPP Law") to carry out the design, financing, construction, operation, and maintenance of Route PY 01 in the Cuatro Mojones – Quiindy section (the "Project").

Project Length

108 km.

Investment Amount

Approximately USD 445,000,000.

Concession Period

30 years.

Design and construction – 44 months.

Operation and maintenance – 26 years and 4 months.

Availability Payment (AP): Fixed payments during the operation stage, updatable and subject to deductions for non-availability and service and quality levels.

Traffic-Linked Payments (TLP): Variable payments subject to traffic demand risk that complement the AP and are based on the traffic effectively counted, based on the existing toll in the city of Itá.

Prequalified Consortia

By Resolution No. 2218 dated December 29, 2023, the MOPC announced the five prequalified consortia that will continue participating in the Tender:

Desarrollo Vial al Sur (Sacyr Concesiones S.L. y Ocho A S.A.)

Rutas del Mercosur (Tecnoedil S.A., Alya Constructora S.A., Construpar S.A. y Semisa Infraestructura S.A.)

AG – Tocsa (AG Construções e Serviços S.A. y Tocsa S.A.)

Rutas del Sur (Cointer Concesiones S.L., Azvi S.A.U. y Constructora Heiseke S.A.)

Rutas del Sur (Acciona Concesiones S.L., Rovella Carranza S.A. y Concret Mix S.A.)

Next Steps

The next step is the opening of the competitive dialogue between the prequalified consortia and the MOPC, during which the parties can discuss the Project's tender documents (e.g., the bidding terms and conditions, the contract, among others). The competitive dialogue phase will conclude with the final version of the Project's tender documents. It is estimated that this stage will take place in February 2024. Finally, it is important to mention that only prequalified consortia can be awarded the Project.

► Drinking water and sanitation project for the Metropolitan Area of Ciudad del Este ("Project”)

General Aspects

The Project aims to tender for works including: (i) the design and construction of a sanitary sewer system, (ii) a wastewater treatment plant, and (iii) improvement of the drinking water system for Ciudad del Este and three neighboring communities. The Project is currently completing the Prequalification Phase No. 784 through which the convener issued Call 58/2023 for expressions of interest for the hiring of consulting services for the oversight of the design and construction of the Project (the "Consultancy").

Project and Consultancy Financing

Inter-American Development Bank (IDB) and Japan International Cooperation Agency (JICA). Approved by Law No. 7088/2023.

Estimated Project Value

USD 200,000,000, of which USD 115,000,000 is granted by the IDB and USD 63,000,000 by JICA; of these, USD 1,600,000 will be allocated for the Consultancy.

Contracting Authority

The MOPC through the Directorate of Drinking Water and Sanitation (the “DAPSAN”).

Modality

International Public Tender.

Legal Framework

Law No. 7021/2022 on Supply and Public Procurement.

Status

The deadline for expressing interest expires on January 24, 2024; after this, the MOPC will form a shortlist of bidders and proceed with the awarding of the Consultancy. The Consultancy is expected to last approximately 45 months.

As for the Project, based on the latest information available, it is likely that the IPT will be called in the first quarter of 2024.

► Drinking Water and Sanitation Project for the Metropolitan Area of Asunción - Lambaré Basin ("Project")

General Aspects

The Project aims to tender for (i) the design and (ii) the construction of sanitary sewer collectors for the Metropolitan Area of Asunción (Lambaré Basin). The Project aims to eliminate 13 discharges of untreated sewage that currently flow directly into the Paraguay River and install a wastewater treatment plant. The Project is estimated to benefit around 300,000 people in the localities of Asuncion, Lambaré, Villa Elisa, and Fernando de la Mora.

Currently, the Project is in the final stages of Prequalification Phase 785 through which the contracting party issued Call No. 60/2023 for expressions of interest in the hiring of consulting services for the supervision of the design and construction of the Project ('Consultancy').

Financing

Inter-American Development Bank (IDB) and the Official Credit Institute of the Kingdom of Spain (ICO). Approved by Law No. 7074/2023. It is worth noting that the financing amount covers the entire project.

Estimated Value

USD 165,000,000, of which USD 2,300,000 will be allocated to the Consultancy.

Contracting Authority

The MOPC through the Directorate of Drinking Water and Sanitation (the “DAPSAN”).

Modality

International Public Tender.

Legal Framework

Law No. 7021/2022 on Supply and Public Procurement.

Status and Next Steps

The deadline for expressing interest expires on January 22, 2024; after this, the MOPC will form a shortlist of bidders and proceed with the awarding of the Consultancy. The Consultancy is expected to last approximately 45 months.

As for the Project, based on the latest information available, it is likely that the IPT will be called in the first quarter of 2024.

► Promulgación de la Ley 7182/2023 que aprueba el contrato de préstamo entre la República del Paraguay y CAF para financiar el proyecto de agua potable, alcantarillado y saneamiento para el Área Metropolitana de Mariano Roque Alonso (“Proyecto”)

General Aspects

The loan granted by CAF will be used for the construction project and system of sanitary sewerage, wastewater treatment plant, and improvement of the drinking water system for the Mariano Roque Alonso basin. The Project's funds are intended for equipment works; acquisition of goods; environmental and social management; supervision and oversight; institutional management and improvement; tax payments; hiring of studies and consulting; audits; and financing of evaluation expenses. The Project's infrastructure includes 447 km of sewerage networks, the construction of a wastewater treatment plant, and 10 pumping and treatment stations.

Financing

CAF – Latin American and Caribbean Development Bank.

Estimated Value

USD 160,000,000, of which approximately USD 151,000,000 will be allocated to the Project works, and the remaining USD 9,000,000 to the administration and management of the Project.

Contracting Authority

The MOPC through the Directorate of Drinking Water and Sanitation (the “DAPSAN”).

Modality

Once the Project is ready, the convener will launch an IPT.

Legal Framework

Law No. 7021/2022 on Supply and Public Procurement.

Status

The IPT is scheduled for the second quarter of 2024.

[1] KIND is an organization founded in 2018 by the Government of the Republic of Korea with the aim of promoting infrastructure projects worldwide under the Public-Private Partnership (PPP) model. Additionally, it supports Korean companies in developing these projects (KIND WEB)

Focusing on crucial tax laws for a comprehensive understanding of the Latin America region, the WSG Tax Group has released a guide providing detailed insights, updates, and trends on a country-by-country basis concerning these laws and policies in the region.

Over 35 tax experts across 17 Latin American jurisdictions have contributed to the guide, serving as a testament to the strength of WSG member partnerships and the highest level of expertise that WSG members bring to key industry updates and trends.

It is worth noting that Rodolfo Vouga, Andrés Vera, and Horacio Sánchez, members of our team, contributed to the chapter on Paraguay.

We invite you to consult the complete guide at the following link.

On December 29th, 2023 the Ministry of Public Works and Communications (MOPC) issued Resolution No. 2218, announcing the five prequalified consortia that will continue participating in the bidding process for Tender 1288 "Call DIPE 01/2023 Prequalification Public Investment Project for the Expansion and Improvement of Route PY01, in the stretch between Cuatro Mojones and Quiindy," covering a distance of 108 km in length (the "Tender").

The Tender is a Public-Private Partnership investment project managed under Law No. 5102/2013 on the "“Promotion of Investment in Public Infrastructure and the Expansion and Improvement of Goods and Services under the State's Responsibility” ("PPP Law") and its regulatory Decree No. 4183/2020.

The next step involves the opening of a competitive dialogue between the prequalified consortia and the MOPC, at which point the parties can discuss the Tender’s documents (e.g., the Terms of Reference, the Contract, among others). It is estimated that this stage will take place in February 2024.

The prequalified consortia are:

Desarrollo Vial al Sur (Sacyr Concesiones S.L. y Ocho A S.A.)

Rutas del Mercosur (Tecnoedil S.A., Alya Constructora S.A., Construpar S.A. y Semisa Infraestructura S.A.)

AG – Tocsa (AG Construções e Serviços S.A. y Tocsa S.A.)

Rutas del Sur (Cointer Concesiones S.L., Azvi S.A.U. y Constructora Heiseke S.A.)

Rutas del Sur (Acciona Concesiones S.L., Rovella Carranza S.A. y Concret Mix S.A.)

To learn more about this project, we invite you to read our previous publications:

A través de la Resolución C.A. 87/2023 (el “Reglamento”) el Instituto de Previsión Social (“IPS”) establece la reglamentación de los requerimientos para la inscripción de asegurados y empleadores (personas físicas o jurídicas, continuidad en el beneficio, y jubilación voluntaria); actualización de datos, reactivación e inactivación de inscripción patronal de personas físicas y jurídicas a través del Sistema Unificado de Apertura y Cierre de Empresas (“SUACE”) del Ministerio de Industria y Comercio (“MIC”).

El Reglamento dispone:

La creación de un Formulario Único de Declaración Jurada de inscripción de empleadores y asegurados, cuyo formato se encuentra como Anexo 3 del Reglamento y que deben utilizarse en los procesos indicados en el punto 3 de este informe.

Cuenta con seis anexos donde se establecen los modelos, y reglamentaciones para la aplicación de este Reglamento.

El Anexo 1 fija los nuevos requisitos y modalidades de inscripción para:

Personas físicas

Personas jurídicas

Sociedades, consorcios, condominios, cooperativas, organizaciones no gubernamentales.

Instituciones educativas privadas.

Organizaciones gubernamentales.

Entidades religiosas.

Embajadas, Cuerpos diplomáticos.

Actividades personales especiales.

Continuidad en el beneficio

Jubilación voluntaria

Trabajadores independientes

Empleadores

Amas de casa

Reactivación patronal y Actualización de datos del empleador

Inactivación patronal

Procedimiento para la formalización de empresas SUACE, que implica la inscripción ante IPS y el MTESS. Fija los requisitos para personas físicas y jurídicas.

El Anexo 2 establece las generalidades para llenado y validez del Formulario Único de Declaración Jurada de inscripción patronal. En líneas generales establece que las documentaciones que deben acompañar el formulario deben ser autenticadas ante escribano público, el formulario debe ser llenado en un color de bolígrafo sin enmiendas ni tachaduras, y debe contener el sello de la empresa (para personas jurídicas), se debe solicitar además el PIN para acceso al Sistema REI. Las solicitudes se procesarán online a través de una plataforma habilitada por el MIC. Una vez culminado se generará el PIN de acceso al Sistema REI.

El Anexo 3 establece el modelo de Formulario Único de Declaración Jurada de inscripción de empleadores y asegurados, actualización de datos, reactivación e inactivación patronal, continuidad en el beneficio y jubilación voluntaria.

El Anexo 4 fija el formulario de registro de firma del empleador y el Anexo 5 dispone el Formulario para inclusión y exclusión de representante legal. La utilización del Registro de Firma del empleador o asegurado deberá realizarlo el funcionario que inscribe para casos excepcionales en el que la firma de estos con coincidan con el documento de identidad, conforme al Anexo 4 y el Anexo 5 del Reglamento.

El Anexo 6 establece el modelo de contrato de adhesión para solicitar el PIN para acceso al Sistema REI.

Autoriza la utilización de fuentes de información provistas por las entidades públicas conforme a la Ley 5655/16 a fin de realizar comunicados, promoción, difusión, procesos administrativos o judiciales a través de los medios que correspondan y actualizar los datos de los empleadores cuando estén incompletos o sean incorrectos.

Ratifica el convenio de cooperación interinstitucional de apoyo al SUACE con los Ministerios intervinientes.

Aprueba el procedimiento online de inscripción patronal de personas físicas y/o jurídicas a través del SUACE por medio de la plataforma informática del MIC.

Excluye de los procesos de formalización de empresas a través del SUACE lo relativo a Continuidad en el Beneficio, Jubilación Voluntaria, Actualización de Datos, y reactivación e inactivación patronal.

El Reglamento dispone:

La creación de un Formulario Único de Declaración Jurada de inscripción de empleadores y asegurados, cuyo formato se encuentra como Anexo 3 del Reglamento y que deben utilizarse en los procesos indicados en el punto 3 de este informe.

Cuenta con seis anexos donde se establecen los modelos, y reglamentaciones para la aplicación de este Reglamento.

El Anexo 1 fija los nuevos requisitos y modalidades de inscripción para:

Personas físicas

Personas jurídicas

Sociedades, consorcios, condominios, cooperativas, organizaciones no gubernamentales.

Instituciones educativas privadas.

Organizaciones gubernamentales.

Entidades religiosas.

Embajadas, Cuerpos diplomáticos.

Actividades personales especiales.

Continuidad en el beneficio

Jubilación voluntaria

Trabajadores independientes

Empleadores

Amas de casa

Reactivación patronal y Actualización de datos del empleador

Inactivación patronal

Procedimiento para la formalización de empresas SUACE, que implica la inscripción ante IPS y el MTESS. Fija los requisitos para personas físicas y jurídicas.

El Anexo 2 establece las generalidades para llenado y validez del Formulario Único de Declaración Jurada de inscripción patronal. En líneas generales establece que las documentaciones que deben acompañar el formulario deben ser autenticadas ante escribano público, el formulario debe ser llenado en un color de bolígrafo sin enmiendas ni tachaduras, y debe contener el sello de la empresa (para personas jurídicas), se debe solicitar además el PIN para acceso al Sistema REI. Las solicitudes se procesarán online a través de una plataforma habilitada por el MIC. Una vez culminado se generará el PIN de acceso al Sistema REI.

El Anexo 3 establece el modelo de Formulario Único de Declaración Jurada de inscripción de empleadores y asegurados, actualización de datos, reactivación e inactivación patronal, continuidad en el beneficio y jubilación voluntaria.

El Anexo 4 fija el formulario de registro de firma del empleador y el Anexo 5 dispone el Formulario para inclusión y exclusión de representante legal. La utilización del Registro de Firma del empleador o asegurado deberá realizarlo el funcionario que inscribe para casos excepcionales en el que la firma de estos con coincidan con el documento de identidad, conforme al Anexo 4 y el Anexo 5 del Reglamento.

El Anexo 6 establece el modelo de contrato de adhesión para solicitar el PIN para acceso al Sistema REI.

Autoriza la utilización de fuentes de información provistas por las entidades públicas conforme a la Ley 5655/16 a fin de realizar comunicados, promoción, difusión, procesos administrativos o judiciales a través de los medios que correspondan y actualizar los datos de los empleadores cuando estén incompletos o sean incorrectos.

Ratifica el convenio de cooperación interinstitucional de apoyo al SUACE con los Ministerios intervinientes.

Aprueba el procedimiento online de inscripción patronal de personas físicas y/o jurídicas a través del SUACE por medio de la plataforma informática del MIC.

Excluye de los procesos de formalización de empresas a través del SUACE lo relativo a Continuidad en el Beneficio, Jubilación Voluntaria, Actualización de Datos, y reactivación e inactivación patronal.

Este contenido tiene únicamente fines informativos generales y no debe ser considerado como asesoría legal puntual. Si precisa asesoramiento específico no dude en contactarnos.

Through Resolution No. 126 dated October 16, 2023, the Secretariat for the Prevention of Money Laundering ("SEPRELAD") approved the procedures and requirements for the deregistration of Obligated Subjects without natural supervision.

Obligated Subjects without natural supervision are understood to be natural or legal persons that are not directly regulated by a government entity. These include:

Pawnshops;

Real estate agencies;

Non-profit organizations ("NPOs");

Money transfer services;

Merchants of jewelry, precious stones and metals, art objects, and antiques; and,

Individuals and legal entities engaged in philatelic or numismatic investment.

According to the new procedure, to deregister due to reasons such as a change in economic activity, dissolution, and/or business closure, Obligated Subjects without natural supervision must submit a request addressed to the highest authority of SEPRELAD requesting deregistration. This request should be accompanied by the Unique Taxpayer Registry ("RUC") certificate, an authenticated copy of the owner's or legal representatives' Identity Card, as well as a certificate of compliance with anti-money laundering and counter-terrorism financing measures issued by the General Directorate of Supervision and Regulation of SEPRELAD. In addition to the aforementioned documents, legal entities that are obligated subjects must submit an authenticated copy of the minutes of the assembly, whether ordinary or extraordinary, in which the suspension or cessation of activity or business closure was discussed. In the case of NPOs, the minutes mentioning dissolution and/or social change should be presented.

Within a maximum period of 10 (ten) business days, the General Directorate of Supervision and Regulations of SEPRELAD will issue the certificate, with the possibility of requesting additional documentation it deems pertinent, leading to the suspension of the stipulated period.

The regulations also consider the possibility of reinstatement for those Obligated Subjects who deregistered, provided they comply again with all the requirements established for registration in the registry of Obligated Subjects without natural supervision of SEPRELAD.