Through Resolution No. 06 Minute No. 02 dated January 17, 2024 (the "Resolution"), the Board of Directors of the Central Bank of Paraguay ("BCP") approved the Standards of Procedures and Minimum Conditions for the Export or Import of Physical Currency.

In this sense, the export or import of physical currency in the Republic of Paraguay must be carried out through transportation and stockpiling companies authorized by the National Police and registered before the Secretariat for the Prevention of Money or Asset Laundering ("SEPRELAD").

Once the Superintendency of Banks ("SIB") verifies that the banking and exchange entities comply with the minimum conditions established in the Resolution, it will grant a general authorization to operate with a specific counterparty and/or foreign banking correspondent in charge of the settlement and payment of the countervalue in a bank account.

Among the minimum conditions established to obtain the SIB's authorization are: (i) Identification of the correspondent banking entities and/or foreign counterparties; (ii) Specification of the countries and cities in which the foreign entities are domiciled; (iii) Submission of evidence that the foreign counterparty entity and the banking correspondent in charge of the settlement of the transactions, are duly authorized; (iv) The foreign correspondent entities and/or counterparties must be subject to a supervision similar to the local one or to the satisfaction of the SIB; (v) Proforma of the contract to be used between the parties where at least the mutual obligations of the parties and the conditions for the provision of the service are established; and, (vi) The banking and exchange entities must prove that both their foreign counterpart and the entity responsible for the settlement of the operations have adequate policies and procedures for the prevention of money laundering, financing of terrorism and proliferation of weapons of mass destruction in their operations. The countries where such entities are domiciled must belong to the Financial Action Task Force or other similar organization.

The MOPC, within the framework of the International Public Tender (IPT) for the National Route Improvement Project No. 17, Road Section between Pedro Juan Caballero – Capitán Bado – Itanará – Ypejhú in the Departments of Amambay and Canindeyú”, has issued Addendum No. 7, postponing the delivery and bid opening dates to April 3, 2024.

February 14, 2024

Call for Bids

The National Directorate of Public Procurement (DNCP) has published on its portal the prequalification for the contracting of design and construction of works for the capture, treatment, and storage of drinking water for the metropolitan area of Ciudad del Este, valued at USD 200,000,000.

February 15, 2024

Call for Bids

The DNCP has published on its portal the prequalification for the contracting of design and construction of the wastewater treatment plant and sub-fluvial emissary for the Lambaré basin, valued at USD 165,000,000.

February 15, 2024

More information

► International Public Tender call for surveying, compensation, expansion, and improvement of Route PY 17 “Route of Sovereignty”

General Aspects

On January 5, 2024, the National Directorate of Public Procurement (DNCP) published on its portal the call for Tender 438107 convened under the IPT procedure for the survey, compensation, construction, and maintenance of the pavement of Route PY 17. This route connects the towns of Pedro Juan Caballero – Zanja Pyta – Capitán Bado – Itanará – Ypejhú, in the departments of Amambay and Canindeyú (the "Project").

The presentation, opening, and award date of the Project had several postponements; the latest was Addendum No. 7 dated March 15, 2024, which establishes that the new deadline for presentation, opening, and, eventually, award of the Project is set for April 3, 2024.

Project Characteristics

Recall that the Project aims to improve the connection between two of the country's most important productive areas. It is estimated that it will benefit around 150,000 people.

The execution of the Project includes, among others, works such as: earthworks, drainage; construction of the structural package, main axis, and accesses; paving; complementary works such as construction and removal of fences, signage, lighting, weighing and toll booths, counting booths, and environmental management plan.

Investment Amount: Gs. 1,432,191,265,000 (Approximately USD 215,000,000). The Project will be financed with a loan from the Financial Fund for the Development of the La Plata Basin (FONPLATA).

Offer Maintenance Guarantee: 3% - policy or bank guarantee.

Adjudication System

Per lot. The Project is divided into 4 lots. The adjudication of more than one lot to an offeror is allowed. Below is the planned length for each lot.

Lot 1 – 44 km

Lot 2 – 48 km

Lot 3 – 53 km

Lot 4 – 48,3 km

Each lot includes all aspects of the Project, i.e., surveying, compensation, construction, and maintenance of the work. The value of each lot is:

Lot 1 – Gs. 377.025.115.000

Lot 2 – Gs. 344.584.917.000

Lot 3 – Gs. 386.590.367.000

Lot 4 – Gs. 323.990.866.000

Approximately USD 53,000,000 on average, depending on the exchange rate.

Award Criteria: The contracting party will award to the bidder who substantially meets the requirements and offers the lowest evaluated price. This is subject to the bidder being considered eligible according to the criteria set forth in the terms and conditions.

Advance Payment: The tender provides for the granting of a 15% advance to the awarded bidders.

Term for execution of works: 24 months from the start order.

Maintenance Period for Service Levels (KPI): 60 months after the completion of the works.

Contracting Systems

Construction works: unit prices

Execution of surveying and expropriations for lands and improvements: provisional sums

Maintenance for service levels: lump sum

Bid validity period: 150 calendar days counted from the deadline for submission of offers.

Offer maintenance guarantee validity period: 180 days counted from the submission of offers.

Bid Submission: National or foreign companies individually or in consortium, with legal, economic-financial, and technical capacity.

Subcontracting: Subcontracting for the execution of some planned works is allowed, but the amount of subcontracted works cannot exceed 40% of the total contract amount. However, the awarded company must obtain prior authorization from the contracting entity.

► Drinking water and sanitation project for the Metropolitan Area of Ciudad del Este ("Project”)}

The Ministry of Public Works and Communications (MOPC) through the Directorate of Drinking Water and Sanitation (DAPSAN) convened Prequalification 787 of the Project on February 15, 2024, which aims to contract the design and construction of works for the capture, treatment, and storage of drinking water in the metropolitan area of Ciudad del Este, the second largest city in Paraguay.

After notification of the prequalification results, the MOPC will invite the prequalified to submit their bids and proposals.

Among the planned works are:

Construction of a water intake chamber with a capacity of 1100 l/s.

Provision and installation of a floating barrier around the intake chamber.

Headworks: Pre-oxidation, Energy Buffer Chamber, Load Chamber, and Overflow Chamber.

Storage of drinking water of 1500m3 within the premises of the Drinking Water Treatment Plant (DWTP).

All civil engineering works must be designed and built for a capacity of up to 1100 l/s and water pump installations capable of delivering a flow of 500 l/s to the distribution center of Presidente Franco.

Construction of a buried cast iron rising main of approximately 900 mm in diameter for an initial capacity of 500 l/s and final project capacity of 1000 l/s.

Construction of 2 reservoirs of 7000 m3 each.

Project and Consultancy Financing: Banco Interamericano de Desarrollo (BID) y Agencia de Cooperación Internacional del Japón (JICA). Aprobada por Ley N° 7088/2023.

Estimated Project Value: USD. 200,000,000 of which USD 115,000,000 granted by the IDB and USD 63,000,000 by JAICA; of these, USD 1,600,000 will be allocated to the Consultancy.

Modality: International Public Tender (IPT).

Relevant dates in relation to the Project

Bid Submission Date: April 22, 2024 (9:00 am).

Bid Opening Date: April 22, 2024 (9:30 am).

Construction Period: 26 months from the receipt of the Project commencement order.

Project Execution Site: City of Presidente Franco, department of Ciudad del Este.

Eligibility Criteria: Companies interested in bidding must demonstrate financial capacity, technical capability, past contract performance/non-performance, among other requirements stipulated in the Project prequalification.

Subcontracting: Subcontracting the entirety of the works is not allowed. However, subcontracting for certain specialized parts of the works is permitted.

► Drinking Water and Sanitation Project for the Metropolitan Area of Asunción - Lambaré Basin ("Project")

The Ministry of Public Works and Communications (MOPC) through the Directorate of Drinking Water and Sanitation (DAPSAN) convened Prequalification 788 of the Project on February 15, 2024, aimed at contracting the design and construction of the wastewater treatment plant (WWTP) and sub-fluvial emissary of the Lambaré basin, a city adjacent to Asunción. The Project is financed with funds from the IDB.

After notification of the prequalification results, the MOPC will invite the prequalified to submit their bids and proposals.

The Wastewater Treatment Plant (WWTP) will require (i) design, (ii) construction, and (iii) provision of:

Dredging of approximately 1,000,000 m3 of sand in an area of 14 hectares and complementary works for stabilization and circulation. Internal and external drains, slope protection, vehicular and pedestrian access to the WWTP. The property must be raised to a level determined by the engineering design of the Project. This is because it is a flood-prone area near the floodplain of the Paraguay River.

Pumping Station 05 (PS05), pumping to the arrival chamber, and complementary works for its connection to the main collector.

Pre-treatment (PT) with odor control and treatment, Bypass (BY), Disinfection (DES emerg), and Sub-fluvial discharge emissary (EMIS).

Provision of electromechanical, electronic, electrical, automation, internal and external security equipment, etc.

Offices, warehouses, operation and maintenance structures, fences, gates, roads, and circulation routes for both vehicles and pedestrians. Personal safety systems and equipment.

Interconnection for access roads to the WWTP with the South Promenade.

Operation and maintenance for a minimum of 1 (one) year of the constructed works and transfer of knowledge to the future plant operator.

Financing: Inter-American Development Bank (IDB) and the Official Credit Institute of the Kingdom of Spain (ICO). Approved by Law No. 7074/2023. It is noteworthy that the financing amount covers the entire work.

Estimated Value: USD 165,000,000, of which USD 2,300,000 will be allocated to Consultancy.

Modality: International Public Tender.

Relevant dates in relation to the Project

Bid Submission Date: April 19, 2024 (9:00 am).

Bid Opening Date: April 19, 2024 (9:30 am).

Construction Period: 52 months plus 12 months of operation and maintenance following the inspection of the works.

Project Execution Site: The works will be carried out in the city of Asunción, and the land where the WWTP will be built is located in the Santa Ana neighborhood with an area of approximately 19 hectares. Additionally, the Sub-fluvial emissary will be executed in the Paraguay River.

Eligibility Criteria: Companies interested in bidding must demonstrate financial capacity, technical capability, past contract performance/non-performance, among other requirements stipulated in the Project prequalification.

Subcontracting: Subcontracting the entirety of the works is not allowed. However, subcontracting for certain specialized parts of the works is permitted.

Other news:

Acquisition of Aircraft for the Paraguayan Air Force

The Government announced its intention to acquire 6 "Super Tucano A 29" combat aircraft from Brazil for the Paraguayan Air Force (FAP). The aircraft would be used to combat organized crime. The investment would be approximately USD 121 million. The amount includes, in addition to the aircraft acquisition, the purchase of weapons, training programs for FAP air personnel, as well as the upgrade of another 6 "Tucano" aircraft of the FAP. The FAP commander indicated that the financing source for the aircraft purchase has not yet been decided; therefore, Government authorities are analyzing various alternatives to make the investment.

Public Hearing Transmission Line 220KV Villa Hayes - Villa Real - Pozo Colorado - Loma Plata and Pozo Colorado Substation

On March 14, ANDE convened a public hearing to present the technical specifications of the construction project of the 220KV transmission line Villa Hayes - Villa Real - Pozo Colorado - Loma Plata and Pozo Colorado Substation. Among the most notable aspects of the hearing, we can mention the following: (i) it is expected that the tender will be launched during this semester; (ii) all lots comprising the tender can be awarded to one or several bidders; (iii) the tender rules will be those of the financier Kreditanstalt fur Wiederaufbau (KfW). The total value of the entire work is approximately USD 120,000,000.

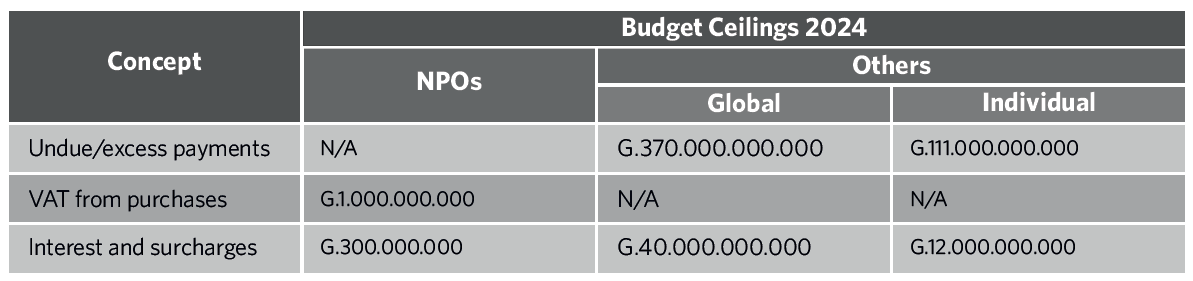

The 2024 budget ceilings are established for the National Directorate of Tax Revenues ("DNIT") to credit amounts for undue or excess payments, interest and surcharges.

December 29, 2023

Law N° 7228

DNIT's budget allocation for fiscal year 2024.

December 29, 2023

Decree N° 1184

The organizational and functional structure of the DNIT.

February 15, 2024

Binding Consultation

The DNIT ruled on the tax treatment to be given to the sale and purchase of goods located abroad between two companies domiciled in Paraguay.

October 2023

More Information:

► Law N° 7228/2023 —The 2024 budget ceilings are established for the DNIT to credit amounts for undue or excess payment, interest and surcharges.

Law No. 7228/2023 approved the General Budget of the Nation ("PGN") for fiscal year 2024 and established several tax measures that, to a greater or lesser extent, affect taxpayers. One of these measures is the annual budget ceilings for crediting taxpayers the balances due to them for:

undue or excess payment, refund of value-added tax ("VAT") from purchases made by non-profit entities ("NPOs"), and

interests in the following tax credit recovery processes:

This budgetary measure has been implemented every year since Law No. 5061/2013 (see Article 7) and Decree No. 850/2013. For this fiscal year 2024, the overall and individual (per taxpayer) budget ceilings are the same as for fiscal year 2023:

The global limits represent the maximum amount that DNIT can credit in the indicated concepts during the entire fiscal year 2024, while the individual limits per taxpayer are 30% of the global limit for each concept. This means that no taxpayer may represent a higher percentage of credits than indicated, thus avoiding the situation where only one taxpayer excludes the others.

These budget ceilings do not apply to the refund of VAT from purchases made by NPOs because of court rulings, as these have their own limits. In addition, the way the latter is credited to NPOs differs from the normal regime, since these amounts are paid in cash, not with credit to the taxpayer's tax account, as occurs in the other cases.

If the total budget ceilings are reached during the fiscal year, the amounts pending crediting are deferred to the following fiscal year without generating legal accessories. The area responsible for making the credits must correlatively record the resolutions that approve the refund for their inclusion in the PGN of the following fiscal year.

► Law No. 7228/2023 - The DNIT budget allocation for fiscal year 2024.

With the approval of the PGN 2024, through Law No. 7228/2023, the DNIT received its budget allocation for that fiscal year. This is also the first budget allocation for the institution since its creation in August 2023, when the former Undersecretariat of State for Taxation ("SET") and the National Customs Directorate ("DNA") were merged.

The DNIT's estimated income for 2024 is G. 990,777,629,187, of which only G.675,694,611,732 (68%, and approx. USD 92.8 million) will be destined for its institutional expenses (this would be its real budget), since G.315,083,017,455 (22%) is a transfer or "contribution" from said institution to the General Treasury, administered by the Ministry of Economy and Finance.

Seen from the point of view of the areas of actions assigned to DNIT, its available budget of G.675,694,611,732 is distributed as follows:

Activity

Amount

%

Administering the internal tax system

G.293.656.247.044

44%

Institutional administrative management

G.135.911.001.821

20%

Collection management

G.24.966.990.225

4%

Controls in secondary zone

G.14.418.633.645

2%

Controls in primary zone

G.35.454.324.981

5%

Customs clearance process

G.171.287.414.016

25%

G.675.694.611.732

100%

Of the resources DNIT has, G.548,905,501,197 (81%) are destined for current expenses and G.125,789,110,535 (19%) for capital expenses. Within current expenses, G.332,491,204,609 (49% of DNIT's actual budget) are allocated to Group 100, Personal Services Expenses (salaries, Christmas bonus, overtime, subsidies, bonuses, etc.).

It is important to highlight that the most significant individual expenditure items correspond to capital expenditures for investments in technology or expenses for its maintenance (Objects of Expenditure 261, 543 and 579), which represent an expenditure of G.108,247,101,103 (16% of DNIT's actual budget).

As a result of the above, the first allocation of the DNIT budget is marked by a strong expenditure on its personnel and information technology, which is consistent with the institutional discourse of betting on its human team and technological equipment.

► Decree N° 1184/2024 - The organizational and functional structure of the DNIT.

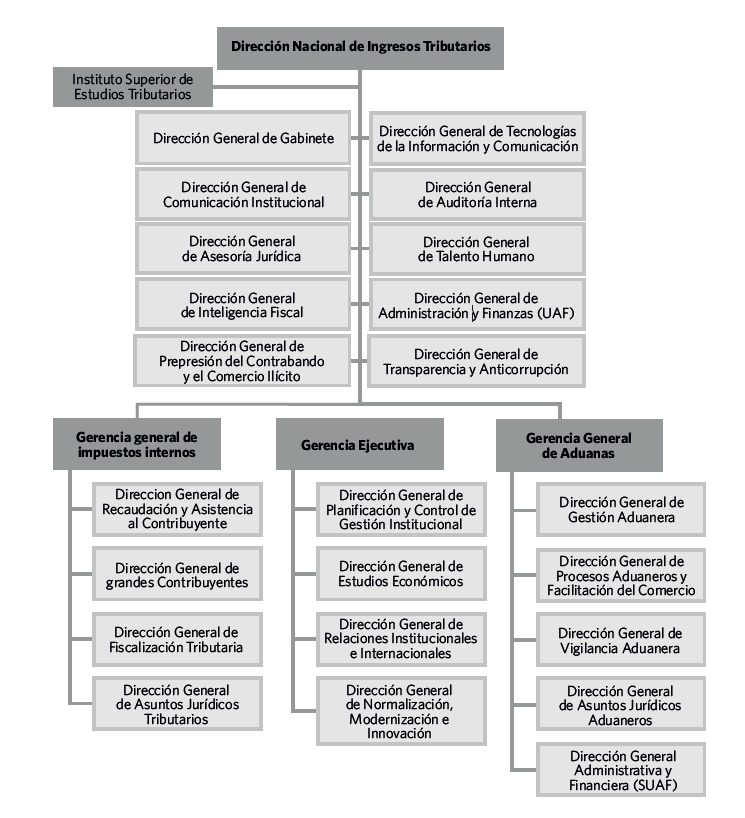

By Decree No. 1184/2024, the Executive Power approved the organizational and functional structure of the DNIT and its divisions, including the 10 General Directorates and the 3 General Managements that report directly to the National Directorate. In this regard, the following diagram (in Spanish) shows the structure of the DNIT:

Among the main changes that can be observed as opposed to the former SET, it can be noted that the now Internal Taxes General Management will have 4 General Directorates out of the 7 that made up the former SET (2 of them became directly dependent of the National Directorate as of Decree No. 82/2013). It is worth mentioning that the former Directorate of Taxpayer Assistance and Tax Credits, as well as the General Directorate of Collection and Regional Offices, have been merged into the General Directorate of Collection and Taxpayer Assistance. Likewise, the former Directorate of Technique and Tax Planning has been renamed the General Directorate of Tax Legal Affairs.

As for the Customs General Management, it will be made up of six of the ten General Directorates that made up the former DNA (3 of them became directly dependent of the National Directorate as from Decree No. 82/2013). On the other hand, the Executive Management will be integrated by 4 General Directorates, which will have among their functions the development of the policies of the DNIT, the representation of the tax administration before international organizations, as well as the collaboration with them in matters of agreements, among others.

Regarding the decree in general, it is worth mentioning that, although it establishes the functions of each of the General Directorates, both those that report directly to the National Directorate and the General Managements, it does not clarify the details of the departments and coordinations that will be part of them, regardless of whether such General Directorates remained unchanged, underwent changes in their functions or were created with this decree. This will likely be regulated by means of a resolution of the DNIT.

► Answer to binding consultation on the tax treatment regarding the transfer of assets located abroad between two companies domiciled in Paraguay.

In response to a binding query during October 2023, the DNIT set forth its position on the tax treatment to be given to the transfer of assets located abroad when such a transaction is carried out by two companies domiciled in Paraguay.

In the consultation filed by the taxpayer, it mentioned that it is a company incorporated and domiciled in the country that is a representative of a Japanese company engaged in the field of engines and spare parts for boats and that it sells such goods to another company also incorporated in Paraguay, for the construction of a ship in Malaysia. In this regard, it was asked whether such purchase and sale transactions and the subsequent delivery of the goods within the national territory are subject to VAT and whether the corresponding invoice should be issued as exempt of this tax.

In this regard, the DNIT concluded that considering that the goods are not in Paraguayan territory when the transactions is carried out, the operation is not subject to VAT since it does not comply with the principle of territoriality necessary for the tax obligation to be born. However, when the vessel assembled abroad incorporates the mentioned goods and is imported to Paraguay, the taxes must be paid for such import, including VAT.

The head of the Vice Ministry of Economy and Planning ("VEP") is appointed as representative of the Ministry of Economy and Finance ("MEF") to the National Council of Free Trade Zones ("CNZF"), replacing the former Undersecretary of State for Taxation ("SET").

December 29, 2023

Decree N° 1032

Decision No. 09/21 of the Common Market Council ("CMC") of the Southern Common Market ("MERCOSUR"), which extends until 2028, the possibility of temporarily increasing the Arancel Nacional Vigente ("ANV") above the Arancel Externo Común ("AEC"), is incorporated to the national legal system.

December 29, 2023

Decree No. 3108

The percentage of guarantees to be presented for the accelerated Value Added Tax ("VAT") refund regime is fixed for 2024.

December 19, 2019 (Update)

Resolutionn- DNIT N° 757 -b

The procedure for the registration of the application for the qualified certificate of electronic signature ("CCFE") in the Marangatú Tax Management System ("Marangatú") is regulated.

January 10, 2024

Resolution DNIT N° 01

The date on which legal entities that register as new taxpayers in the Taxpayer Registry ("RUC") are obliged to issue their receipts only electronically is postponed until January 1, 2025.

January 12, 2024

► Decree No. 1026/2023 - The head of the VEP is appointed to represent the MEF that integrates the CNZF, replacing the former SET.

By means of Decree No. 1026/2023, the Executive Branch amended Article 1 of Decree No. 7713/2000, by which the CNZF was integrated, to appoint the head of the VEP as representative of the MEF that integrates the CNZF. Thus, the position previously held by the head of the former SET, an institution that has been absorbed by the National Directorate of Tax Revenues ("DNIT"), was replaced.

This is because Law No. 523/1995 establishes that the CNZF will be composed of three members, each representing the following ministries: (1) Ministry of Finance ("MH") (replaced by MEF), (2) Ministry of Industry and Commerce, and (3) Ministry of Public Works and Communications.

This implies that the tax authority, which today is the DNIT, no longer occupies a seat within the CNZF since, unlike the former SET -which depended on the former MH-, the DNIT is an autonomous entity and is not part of the structure of the MEF. Something similar happened in 2004 when, with the Customs Code entry into force contained in Law No. 2422/2004, the customs authority ceased to participate in the CNZF when the former National Customs Directorate was separated from the SET and, thus, from the MH.

The question remains as to whether, in the near future, a new seat will be created in the CNZF, to be occupied by a representative of the new tax and customs authority, especially taking into account the special tax regime that free zone users have and the inspection and control tasks that the DNIT must exercise over them.

► Decree No. 1032/2023 - Decision No. 09/21 of the MERCOSUR CMC, which extends until 2028 the possibility of temporarily increasing the ANV above the CET, is incorporated into the national legal system.

By means of Decree No. 1032/2023, the Executive Power has incorporated into the national legal system Decision No. 09/21 (the "Decision") of the MERCOSUR CMC on “Specific actions in the tariff area due to trade imbalances derived from the international economic situation", which has already been protocolized before the Latin American Integration Association ("ALADI"), as the fourteenth (214.o) additional protocol to the Economic Complementation Agreement No. 18 of 1991.

The decision extends until December 31, 2028, the mechanism established in Decision No. 27/15 of the CMC, by which MERCOSUR States Parties may request a transitory increase of the import tax rates or ANV above the CET for imports from outside the MERCOSUR zone, which was only in force until December 31, 2021. Likewise, the mechanism foresees the process by which the States Parties may object to the increase sought by another.

It is worth mentioning that the rate increases intended by a State party may not exceed the maximum bound by the other States party to the World Trade Organization ("WTO"); they may not exceed 100 tariff positions of the Common Nomenclature of Mercosur ("NCM"), nor may they have a duration of more than 12 months, extendable for equal periods. The intended elevations of the ANV and its extensions must be submitted to the consideration of the other States Parties through the Pro Tempore Presidency of Mercosur, which is currently held by Paraguay.

It is important to mention concerning MERCOSUR tariff regulations that recently, in December 2023, MERCOSUR has decided to extend until December 31, 2025, the suspension of restrictions to the List of Exceptions to the Common External Tariff ("LETEC") of each State Party, through Decision No. 12/23 of the CMC. This restriction meant that the States could only modify up to 20% of the NCM codes of their respective LETECs every six months. With the suspension of this restriction, States may modify 100% of the NCM codes of their LETECs, which for Paraguay means the possibility of modifying the 649 NCM codes foreseen for its LETEC.

► Decree No. 3108/2019 - The percentage of guarantees to be submitted for the accelerated VAT refund regime is fixed for 2024 (UPDATE).

Article 102 of Law No. 6380/2019 had foreseen that exporters and freight forwarders may request an accelerated refund of the VAT credit affected their export or export freight operations, presenting for this purpose a bank guarantee, financial guarantee or insurance policy with a minimum validity of 90 business days from the date on which the refund request is filed.

For the first three refund requests under the accelerated regime, the guarantee must cover 100% of the VAT credit capital required to DNIT, plus accessories. From the fourth application onwards, the guarantee must only cover the portion of the VAT credit resulting from the average percentage of rejected credits ("PCR") under the accelerated regime form January to November of the previous year, plus accessories.

To establish the value of the guarantee, the applicant must multiply the PCR by the VAT credit for which a refund is requested. The following legal accessories must be added to the resulting amount, calculated up to the expiration date of the guarantee on the amount of the VAT credit resulting from the PCR: daily interest of 0.05% and late payment penalty of 12%.

DNIT publishes the annual PCR; on this occasion, it was published that the PCR is 3.48% for 2024. This PCR represents an increase of 173 basis points (+1.73%), which is almost a doubling of the PCR set for 2023, which was 1.75%. DNIT accompanied this publication with the following example calculation for the guarantee:

Data

Securities

Amount requested:

₲1,500,000,000

Date of application:

08/01/2023

Warranty issued:

08/01/2023

Warranty expires:

21/05/2023

PCR:

3,48%

Exercise

VAT credit:

₲52.200.000

= ₲1.500.000.000 x 3,48%

Interest:

₲3.497.400

= ₲52.200.000 x 134 x 0,05%

Overdue:

₲6.264.000

= ₲52.200.000 x 12%

Warranty:

₲61.961.400

A more direct way to express the total coverage of the guarantee as a percentage of the VAT credit is achieved by expressing the accessories as percentages of the PCR. This is achieved by estimating the interest at 6.7% (134 days times 0.05%) and the late payment penalty at 12%, which, when added together, amount to 19.7% of the PCR, which can be rounded up to 20%. To add this percentage directly to the PCR, it must be expressed as 1.20 times the PCR, which for a PCR of 3.48% means a total guarantee of 4.18% of the VAT credit.

In those cases where the bank, financial or insurance policy guarantee is less than the amount rejected, the taxpayer must immediately pay the difference in favor of the Treasury, plus the legal accessories that will be calculated until the total payment.

► Resolution DNIT N° 757/2024 - Regulates the procedure for registering the CCFE application in Marangatú.

Through Resolution DNIT No. 757/2024 regulates the procedure for registering the CCFE application through Marangatú. While the application is made before the DNIT, the issuance of the certificate will be performed by a Qualified Provider of Trust Services ("PCSC"). The DNIT acts as an intermediary between the interested party and the PCSC and apparently absorbs the costs of the CCFE.

To apply for the CCFE, the interested party must appear in person at the DNIT office and must comply with the following requirements:

To have the RUC in active status.

Have declared in the RUC the following contact information: (i) a cell phone number, (ii) an e-mail address and (iii), in the case of legal entities, the name and surname of the leading legal representative with the above data for this representative.

To have a confidential access password to Marangatú (Form N° 625 - Act of Manifestation of Will in "Approved" status).

Be up to date in the fulfillment of their tax obligations.

Submit the original documents, according to the type of person concerned, which must match the documents stored in the Marangatu, which are as follows:

Individuals, Individual Limited Liability Company ("EIRL") and undivided succession.

Legal entities and other types of entities

A valid identity card or passport issued in Paraguay.

An identity card or valid passport is issued in Paraguay by the leading legal representative of the legal entity.

The deed of incorporation is duly registered in the Public Registry of Commerce (applicable for EIRL).

Specific documents required according to the type of legal entity (these are detailed in the annex to the resolution).

An original or copy authenticated by a public notary of the resolution of declaration of heirs (applicable for inheritance).

Once the DNIT official, who acts as a registration agent, verifies compliance with the requirements indicated, it will proceed to register Form No. 16, "Request for Qualified Electronic Signature Certificate", in the Marangatú. Subsequently, the applicants will receive a link in the Marandu mailbox, redirecting them to the user portal, where they must request the certificate and create a key for their electronic signature.

The PCSC will forward the contract to the DNIT to provide trust services and issue the CCFE in its system. The contract will be printed so that the applicant can sign it; then, it will be digitized and stored within Marangatu.

The CCFE will be valid for four years from the date of issuance and may be renewed or revoked at the taxpayer's request. After the term above has elapsed without renewal, the CCFE will be extinguished due to expiration. The request for renewal of the CCFE must be made within 30 days before the expiration date, for which the taxpayer must comply with the same requirements mentioned above to obtain the CCFE.

The DNIT will gradually establish the taxpayers who must comply with Resolution DNIT No. 757/2024 provisions to obtain the CCFE for the improvement of tax management.

► Resolution No. 01/2024 - The date on which legal entities registering as new taxpayers in the RUC must issue their vouchers only electronically was postponed.

By means of General Resolution DNIT No. 01/2024, it was established that as of January 1st, 2025, legal entities that register as new taxpayers in the RUC may only issue their receipts electronically, through the E-Kuatia system or the E-Kuatia'i system, except the virtual withholding voucher.

To guarantee this measure, the resolution also establishes that, as of the date above, the DNIT will no longer issue stamps to generate receipts that are different from the electronic ones, also exempting from this measure the virtual withholding voucher.

This modifies the provisions of General Resolution No. 105/2021, which had established January 1st of this year as the starting date of the measure. The reason responds to the objective of achieving a sustainable and gradual implementation of the Integrated National Electronic Invoicing System ("SIFEN"), whose general regulations were recently updated in December 2023 by Decree No. 872/2023.

This amendment also defers the generalized application of electronic invoicing until after the mandatory calendar provided for in Article 1 of General Resolution SET No. 105/2021 is exhausted, whose last date of application, foreseen for Group 10 in the mandatory scheme, is set for October 1st, 2024. Thus, the new taxpayers affected by this modification would become a sort of Group 11 of electronic invoicing.

A través de la Resolución C.A. N° 010-001/2024 (la “Resolución”) el Instituto de Previsión Social (“IPS”) actualiza el haber mínimo de jubilaciones y pensiones de los beneficiarios del IPS, incrementándolo en un 5,1%.

La Resolución dispone:

La fijación de los nuevos valores del haber jubilatorio, como sigue:

Amount

Gs. 884.523

Gs. 1.340.187

Gs. 2.010.280

% del SML – Gs. 2.680.373

33%

50%

75%

Sujetos

• Beneficiarios del sistema de intercajas, los jubilados y pensionados conforme a los convenios internacionales • Beneficiarios de una jubilación por invalidez temporal.

• Beneficiarios de pensiones a derechohabientes

• Beneficiarios de jubilaciones por vejez. • Beneficiarios de una jubilación por invalidez permanente o definitiva.

El pago retroactivo del haber mínimo de jubilaciones y pensiones con los valores indicados anteriormente, a partir del 1 de julio de 2023, para aquellos beneficiarios cuyos beneficios iniciaron antes de dicha fecha, y, desde la fecha de inicio del beneficio para quienes se han jubilado posterior al 1 de julio de 2023.

Este contenido tiene únicamente fines informativos generales y no debe ser considerado como asesoría legal puntual. Si precisa asesoramiento específico no dude en contactarnos.

Vouga Abogados assisted CAF - Development Bank of Latin America and the Caribbean in the granting of a USD 30 million credit line to Banco Continental S.A.E.C.A

The funds provided to Banco Continental S.A.E.C.A. will be used to finance small and medium-sized enterprises (SMEs). This transaction is significant not only due to the considerable amount of funds involved but also because of its role in fulfilling the vital need for capital to fuel the development of businesses that constitute the backbone of Paraguay's economic landscape. This contributes to the business development of our country.

The firm played an integral role that ranged from advising CAF during the negotiation of the credit line contract with the local bank to assisting in drafting the financing documents, conducting due diligence for the bank, and its initial disbursement.

Cynthia Fatecha and Carlos Vouga led the team in providing guidance, supported by associates Belén Rodríguez and Lucas Rolón.

For further information regarding this transaction or other topics related to Banking & Finance, please feel free to contact Carlos Vouga (cvouga@vouga.com.py)

With the enactment of Decree No. 1188/2024, which approves the Financial Plan and the execution of Paraguay’s General Budget of Expenditures 2024, the DNCP announces a significant milestone for bidders, suppliers of the State and, public entities alike. As of Monday, February 19, 2024, Law 7021, and its regulatory decree No. 9823/2023 ("Decree 9823") will apply to all public procurement processes, fully replacing, after more than 20 years, Law 2051/2003. Although Law 7021 became fully effective with the enactment of Decree 9823, some processes were still governed by the previous law since the innovations introduced by the new regulatory framework required technical adjustments for its full application. In this regard, since August 2023, the DNCP has dedicated efforts to implement technological modules adapted to the new legislation. In addition, the DNCP has worked on the elaboration of regulatory administrative resolutions that are essential for the effective application of Law 7021 and Decree 9823.

To access detailed information on the regulatory framework, the complete regulatory index is available at the following link: Law 7021 and Decree 9823; DNCP Resolutions In addition, a new decree is expected to be enacted in the coming weeks, expanding and modifying Law 7021.

Vouga Abogados advised CAF - Development Bank of Latin America and the Caribbean, in the granting of a USD 50 million credit facility to the Financial Development Agency (AFD for its acronym in Spanish), which is the sole second-tier public bank in Paraguay. The funds obtained by the AFD will be used to finance working capital, investments, economic activities linked to the agro-industrial sector, foreign trade operations, and partial guarantees for AFD bond issuances.

The firm's role encompassed negotiating the credit line contract with the state entity, drafting financing documents, and conducting due diligence for the AFD.

Cynthia Fatecha and Carlos Vouga led the team in providing guidance, supported by associates Belén Rodríguez and Lucas Rolón.

For further information regarding this transaction or other topics related to Banking & Finance, please feel free to contact Carlos Vouga (cvouga@vouga.com.py)

Por medio de la Resolución CA N° 005-013 de fecha 24 de enero de 2024 (la “Resolución”), el IPS estableció:

La exoneración del monto en concepto de recargo por mora para los empleadores aportantes del Régimen especial y general sobre planillas normales, planillas complementarias y/o cuotas de fraccionamientos de pagos vencidos e impagos, con vigencia hasta el 30 de abril de 2024.

La Resolución establece la exoneración como sigue:

Del 100% del monto en concepto de recargo por mora en la modalidad de pagos al contado de la totalidad de lo adeudado.

Del 50% del monto en concepto de recargo por mora en la modalidad de pagos parciales.

Durante la vigencia de la Resolución queda suspendida la Resolución CA N° 020/2021 respecto a los recargos por mora para el pago de aportes vencidos e impagos.

Los empleadores que gestionen fraccionamientos a través del Sistema REI en cualquier modalidad de financiación serán liquidados con los cálculos de los recargos legales conforme a las reglamentaciones vigentes.

Respecto de los empleadores que cuenten con certificados de deudas sin procesos judiciales o con trámites judiciales ya iniciados por el IPS y soliciten acogerse a los beneficios de esta Resolución, se procederá de la siguiente manera: (i) desbloqueo de cuenta; (ii) cobro de aportes vencidos, y (iii) posterior comunicación a la dirección jurídica del IPS.

El IPS adecuará los sistemas informáticos para la implementación de lo dispuesto en la Resolución.

Este contenido tiene únicamente fines informativos generales y no debe ser considerado como asesoría legal puntual. Si precisa asesoramiento específico no dude en contactarnos.

On February 12, 2023, the Executive Branch promulgated Decree No. 1168/2024 (“Decree 1168/24”) which regulates Law 6977/2023 "QUE REGULA EL FOMENTO, GENERACIÓN, PRODUCCIÓN, DESARROLLO Y LA UTILIZACIÓN DE ENERGÍA ELÉCTRICA A PARTIR DE FUENTES DE ENERGÍAS RENOVABLES NO CONVENCIONALES NO HIDRÁULICAS" (“Law 6977/23”).

Decree 1168/24 regulates, among other aspects, the following:

The processes for obtaining the various types of licenses for Non-Conventional Renewable Energies (NCRE) provided for in Law 6977/2023 (such as: NCRE Self-generator; NCRE Generator; NCRE Exporter; NCRE Cogenerator), as well as their duration and the grounds for their cancellation;

The regulation applicable to each type of NCRE license and its related activities;

The incentive regime applicable to NCRE licensees; and,

The dispute resolution regime between licensees and the State.

Other important aspects, such as the formula for the NCRE Reference Tariff (the tariff that the State must pay to licensees – except for the NCRE Exporter – for the acquisition of electric energy) will be established through administrative resolutions of the implementing authority, the Ministerio de Obras Públicas y Comunicaciones (Paraguay’s Ministry of Infrastructure) through the Viceministerio de Minas y Energía (Deputy Ministry of Mines and Energy).

To access the full text of Decree 1168/24 click here.

For more information on Decree 1168/24 and Law 667/23 or any other aspect related to the Energy sector in Paraguay, please contact our partners: Rodolfo G. Vouga (rgvouga@vouga.com.py) and Manuel Acevedo S. (macevedo@vouga.com.py)