Through Resolution No. 1 dated September 2, 2025, the Central Bank of Paraguay updated the Regulation on Transparency and Minimum Criteria for the Collection of Fees, Charges, and Penalties in the Financial System (the “Regulation”).

The Regulation introduces a new chapter specifically addressing automatic debits, applicable to all entities supervised by the Superintendency of Banks (“SIB”). Among the key updates are the prohibition on including irrevocability clauses in debit authorizations and the possibility for clients to suspend or revoke the service by any reliable means up to 48 hours prior to the due date.

In addition, supervised entities must assign a unique identification number to each credit operation, which must appear in the contract, settlement, promissory note (pagaré), and any other related document. The Regulation also requires the implementation of mechanisms to ensure the effective cancellation of originating documents once the credit has been settled. This obligation must be incorporated into each entity’s operational manuals, including a specific timeframe for compliance. The SIB may also issue standardization rules regarding the unique identification of credit operations.

Regulates Law No. 4535/2025 for Micro, Small, and Medium-Sized Enterprises (“ “MIPYMES” for its initials in Spanish”)

Decree No. 4638/2025

September 18, 2025

Paraguay incorporates a new regime of origin within the framework of the Sixty-Ninth (69th) Additional Protocol to Economic Complementation Agreement (“ACE”) No. 35 between the Southern Common Market (“MERCOSUR”) and Chile.

General Resolution No. 36/2025

September 11, 2025

The National Tax Revenue Directorate (“DNIT”) established administrative measures for guarantee trusts.

September – 2025:

► Decree No. 4535/2025 – Law No. 4457/20l2 on MIPYMES is regulated.

The Executive Branch issued Decree No. 4535/2025, which regulates the recently amended and expanded law on the promotion of MIPYMES. The new regulations reinforce the state's commitment to the formalization, competitiveness, and sustainability of a sector that represents the majority of the country's business fabric.

The decree consolidates the role of the Ministry of Industry and Commerce (“MIC”), through its Vice Ministry of MIPYMES, as the authority responsible for coordinating public policies for the development of the sector. Under its direction, a National MIPYMES System is created, which will integrate public, private, and academic entities to implement training, technical assistance, innovation, and access to financing programs.

One of the central points of the regulation is the official classification of MIPYMES, which is established according to their level of turnover and number of workers:

Category

Employees

Annual Turnover

Microenterprises

≤ 10

≤ $ $ 1 billion

Small businesses

11-30

≤ G. 5 billion

Medium-sized companies

31-50

≤ G. 10 billion

This classification is the basis for access to benefits and support programs, as well as for inclusion in the new National Registry of MIPYMES ("RENAMIPYMES"), which will issue the MIPYMES Card, a digital document that certifies formal MIPYMES status and allows access to government incentives.

The decree also regulates the differentiated tax and labor regime introduced in Law No. 7444/25, which provides the following benefits for micro and small enterprises with respect to mandatory taxes related to the exercise of their respective economic activity, corresponding to services provided for registration and authorization by central government agencies and decentralized entities:

Seniority:

≤ 3 years

> 3 years

Microenterprises

Exemption

75% discount

Small businesses

N/A

80% discount

In the labor sphere, more flexible contractual arrangements and a transitional regime are being introduced, allowing micro-enterprises to pay 80% of the minimum wage during their first three years of formal operation.

The regulation also promotes the simplification of procedures through the Unified System for Opening and Closing Businesses (“SUACE”), the digitization of administrative processes, and the creation of financial support mechanisms such as the FONAMIPYMES trust, designed to facilitate access to credit and operating capital.

With these regulations, the State seeks to create a more agile and accessible environment for MIPYMES, promoting their formal growth, financial inclusion, and active participation in the national economy.

► Decree No. 4638/2025 – The 69th Additional Protocol to ACE No. 35 between MERCOSUR and Chile is incorporated into the national legal system.

The Executive Branch issued Decree No. 4638/2025, incorporating into national law the 69th Additional Protocol to ACE No. 35, concluded between the States Parties of MERCOSUR and the Republic of Chile. With this measure, Paraguay updates and harmonizes its regulations on rules of origin, completely replacing Annex 13 of the ACE and its previous amendments.

The new text seeks to modernize the regulatory framework governing trade between MERCOSUR and Chile, adapting it to the current needs of operators and aligning it with international standards on trade facilitation. In this regard, more precise definitions, simplified administrative processes, and a clearer procedural structure are introduced, resulting in greater legal certainty and predictability for economic agents.

The Rules of Origin included in the Protocol establish the criteria that determine when a product can be considered originating and, therefore, benefit from the tariff preferences of the agreement. Among the main amendments are the following:

Updating of the rules of origin: The criteria under which a product is considered to be originating in MERCOSUR or Chile are specified, including the tariff jump (first four digits of the tariff nomenclature) for granting the origin regime. This tariff jump may be waived if the CIF value of non-originating materials used in the production of the goods does not exceed the respective tolerance margins of the FOB value of the finished product (40% in general and 45% for certain products).

New specific origin requirements: For certain agricultural, food, and industrial products, detailed technical requirements (such as the use of regional raw materials or specific manufacturing processes) are established that must be met in order to access the preferences of the agreement.

Recognition of digital certificates of origin: The protocol grants full legal validity to certificates issued electronically and digitally signed by authorized certifying entities. This represents a significant step toward the digitization of regional foreign trade, reducing administrative costs and time.

Strengthening of control and verification procedures: Clear rules are established on record keeping, the submission of sworn statements of origin, deadlines for verification by customs authorities, and mechanisms for cooperation between competent authorities. Verifications may even be carried out through visits to the premises of exporters or producers, under regulated conditions and with respect for the confidentiality of information.

Accumulation and flexibility mechanismsThe possibility remains for materials originating in any signatory country to the ACE to be considered as originating in the other countries. In addition, a differentiated origin regime favorable to Paraguay (50% tolerance margin) is incorporated until 2038, with the possibility of automatic renewal for successive 5-year periods, which is applicable to parts of chapters 38, 39, 61, 62, 62, 85, 87, 94, and 95 of the tariff nomenclature.

Transition and repeal of previous rulesThe new protocol repeals the previous ones (58th, 63rd, 65th, and 68th) that amended the same annex, unifying the current provisions on origin into a single text. This facilitates the practical application of the regime and eliminates inconsistencies arising from overlapping rules.

The Additional Protocol will enter into force sixty days after the Latin American Integration Association ("ALADI") notifies the signatory countries of the receipt of formal notifications of compliance with the internal procedures of each State Party. At the national level, the MIC will be the authority responsible for its implementation and coordination, together with the other public institutions competent in customs and trade matters.

With this incorporation, Paraguay reaffirms its commitment to regional economic integration, trade liberalization, and the harmonization of rules that promote a more competitive and predictable environment for businesses. The new rules of origin regime is a key tool for strengthening the country's participation in regional value chains and improving access conditions for Paraguayan products to the Chilean market and other MERCOSUR partners.

► General Resolution No. 36/2025 - Administrative measures were established for guarantee trusts.

The DNIT issued General Resolution No. 36/2025, which establishes new administrative measures applicable to guarantee trusts, with the aim of facilitating their identification and simplifying compliance with their tax obligations.

This resolution extends to all guarantee trusts the special conditions that previously only benefited those established under the "Che Róga Porã" program, thus seeking to standardize the administrative treatment of this type of fiduciary structure.

Guarantee trusts are considered transparent legal structures under Law No. 6380/2019, and therefore they usually register for Corporate Income Tax ("IRE") and Value Added Tax ("VAT") obligations. However, in practice, they only record economic movements at the beginning and end of the contract, remaining inactive for most of its term.

The DNIT seeks to reduce the operational burden involved in filing monthly returns with no movement and recording receipts. Consequently, the resolution introduces a more streamlined procedure adapted to the nature of these financial instruments. Among the main provisions are:

Registration in the Single Taxpayer Registry ("RUC”): Guarantee trusts must register only with the annual obligations of General IRE - Code No. 700 and "Annual Receipt Registry" - Code No. 956, thus eliminating the monthly administrative burden of document filing and VAT.

VAT return: These trusts will only have to settle and file VAT returns in periods when there are operational movements, eliminating the obligation to file monthly returns without activity. It will not be necessary to maintain the General VAT obligation (code 211) active in the RUC.

Adjustment of already registered trusts: Guarantee trusts that are already registered must cancel the General VAT obligation and the monthly receipt registration, replacing them with the annual registration. This transition must be accompanied by the declaration of closure of the canceled obligations, corresponding to the last fiscal period affected.

The new regime represents a significant step forward in terms of administrative simplification, as it adapts the formal requirements of the DNIT to the operational reality of guarantee trusts. These measures reduce compliance costs and times, benefiting both trustees and trustors who bear the costs of the trust business. In addition, the scheme reinforces the traceability and control of trust movements through digitized annual records, maintaining fiscal transparency without imposing unnecessary burdens.

The Senate approved a bill to reform of the metropolitan public transport service.

Start Orders

August 26, 2025

The Ministry of Public Works and Infrastructure (“MOPC”) issued commencement orders for the construction of sanitary sewer systems in 3 cities as part of a sanitation program. Value of the project: USD 40 million.

Call for Bids

September 12, 2025

The National Directorate of Public Procurement (“DNCP”) published on its official website an International Public Tender (“LPI”) for the paving of Route PY12 (Cruce Colonia Margarita – Itakyry section), convened by the MOPC.

Bill

July 24, 2025

The Executive Branch submitted a bill to merge the Ministry of Industry and Commerce, the Vice Ministry of Mines and Energy and the National Secretariat of Tourism into the new Ministry of Industry, Commerce, Tourism, Mines and Energy.

Project Socialization

August 19, 2025

The MOPC launched the public consultation process for the tender of the project to improve urban access to Route PY01. Value of the project: USD 180 million.

Award

September 23, 2025

The MOPC announced the awarding of International Public Tender No. 3101, for the improvement and duplication of Route PY01 on the Cuatro Mojones – Quiindy section, which will demand investments estimated in over USD 400 million..

Call for Bids

September 30, 2025

National Directorate of Public Procurement (“DNCP”) published National Public Tender ID No. 475451 for the execution of maintenance dredging works on the Paraguay River along the section from the Paraná River confluence to the Apa River mouth.

More Information:

I. The Senate Approves with Amendments a Law Reforming the Metropolitan Public Transport Services

On July 24, the Executive Branch, through the Ministry of Public Works and Communications (MOPC), submitted to the National Congress the bill entitled “Establishing Oversight of Land Transportation and Amending and Expanding Provisions of Law No. 1590/2000 Relating to the Metropolitan Public Passenger Transport Service” (the “Bill”). The Bill seeks to redefine the metropolitan public transport service and, at the same time, reorganize the sector’s oversight through the creation of a modern institutional framework.

A. Institutional Framework

El Proyecto de Ley establece que la prestación de los Servicios de Transporte Público Metropolitano (“Servicios”) se organizará mediante contratos de concesión adjudicados por el MOPC a través de licitaciones públicas. Los Servicios a ser concesionados incluyen:

fleet supply contracts,

infrastructure supply contracts,

fleet operation services, and

complementary services.

Fleet supply, fleet operation, and complementary service contracts may be awarded for terms of up to 15 years, while infrastructure supply contracts may extend up to 20 years.

The Bill also allows concession contracts to include arbitration as a dispute resolution mechanism for matters of a private nature, thereby introducing higher predictability standards for international stakeholders.

B. Financing and Tariff Scheme

The Bill establish a Financing Administration Trust with segregated assets to be managed managed by the Development Finance Agency (Agencia Financiera de Desarrollo or AFD) (the “Trust”)acting as trustee and the MOPC as trustor. The Trust is aimed exclusively at ensuring timely payments to service providers. This mechanism seeks to reduce liquidity risks and enhance the system’s financial stability.

The Trust’s funds may be carried over between fiscal years and must cover firm liabilities for a minimum of 12 months, according to the contractual schedule. Revenues from the electronic ticketing system will be transferred daily to the Trust, which will in turn pay the operators as instructed by the MOPC. Additionally, internal and external audits are established, including the oversight by the Office of the Comptroller General of the Republic (CGR), to ensure transparency and proper management of resources.

Regarding fares, the Executive Branch will set user tariffs based on MOPC proposals, taking into account criteria such as : affordability, sustainability, and equity. Provider’s compensation may be calculated based on variables such as kilometers traveled, passengers transported, or fleet and infrastructure availability, as well as service levels and performance indicators. To safeguard economic balance, remuneration will be subject to automatic adjustment mechanisms through polynomial formulas linked to relevant cost evolution, thus providing long-term revenue certainty.

C. Technical and Sustainability Conditions

The Bill introduces a maximum age of 15 years for fleet units, requiring the progressive renewal of buses in service. Likewise, it also authorizes mandates for low- or zero-emission vehicles, opening space for investment in new technologies and sustainable mobility solutions.

The Bill also allows the State to acquire bus fleets and infrastructure for the service and to operate them under different contractual schemes—leasing, commodatum, usufruct, management trusts, financial leasing, or others—depending on the public interest. For electric or hybrid buses and their charging infrastructure, direct pilot agreements with specialized providers are contemplated.

A special regime is also created for assets allocated to the service, requiring registration in a dedicated registry, setting out rules for dereservation upon contract termination, and establishing protections to limit attachment or enforcement by creditors, thereby strengthening operational security .

Furthermore, the mandatory interoperability of electronic ticketing systems with multiple payment methods is introduced, encouraging technological innovation in the user experience and creating opportunities for digital service providers.

D. Guarantee of Service Continuity

From the users’ perspective, the Bill guarantees continuous provision of the service even in the event of strike , by establishing minimum coverage percentages. It also reinforces users’ rights through the establishment of quick and accessible complaint mechanisms and granting the regulator broad supervisory powers to ensure the quality and safety of the service.

E. Legislative Process

The Bill was approved by the Senate, the chamber of origin, on September 9, 2025, and is currently pending before the Chamber of Deputies for its second constitutional review. The Bill is available at the following here.

II. Progress of the Sanitation Program for Intermediate Cities

MOPC recently issued commencementorders for the construction of sanitary sewer systems in 3 of the 4 cities included in the Sanitation Program for Intermediate Cities (the “Program”), financed by the Development Bank of Latin America and the Caribbean (CAF). The cities are: Santa Rita (Alto Paraná), San Ignacio Guazú (Misiones), and Carapeguá (Paraguarí).

The Program aims to expand sewer network coverage, optimize wastewater treatment, and improve the drinking water supply. The Program also encompasses the construction of collection networks, pumping stations, household connections, and wastewater treatment plants (WWTPs), enabling effluents to be returned to the environment under safe and sustainable conditions. More than 120,000 people in the four selected cities are expected to benefit.

The contracts for the works were awarded through International Public Tender No. 33/24 for a total value of approximately ₲ 358,937 million (approximately USD 50 million), to the following companies:

In Santa Rita, to Construcciones y Viviendas Paraguayas S.A. (COVIPA) with an investment of ₲ 82,459 million (approximately USD 11.5 million).

In San Ignacio Guazú, to the Rovella-TOCSA Consortium, with an investment of ₲ 114,423 million (approximately USD 16 million).

In Carapeguá, to the Carapeguá Sanitation Consortium. The investment will amount to ₲ 87,004 million (approximately USD 12 million).

The execution of the works will be overseen by the Directorate of Drinking Water and Sanitation (DAPSAN), a division of the MOPC. Completion and delivery are scheduled for July 2028.

The Project marks a significant step in strengthening tParaguay’s sanitation infrastructure, not only by expanding coverage in intermediate cities facing growing urban demand, but also by creating opportunities for the private sector in areas such as engineering, construction, equipment supply, and the operation of related services.

III. Tender for the Paving of Route PY21: Cruce Colonia Margarita – Itakyry Section

General Overview

On September 12, 2025, MOPC, through the National Directorate of Public Procurement (DNCP), published International Public Tender No. 468137 corresponding to MOPC Call No. 94/2025 (the “Project”). The Project involves the asphalt paving of a 26.5 km section of Route PY21, which connects Cruce Colonia Margarita with the city of Itakyry, in the department of Alto Paraná.

The Project is designed to facilitate the transportation of goods along this corridor while improving access to healthcare and educational centers.

Key Features

Project Value and Financing The works are estimated at ₲ 134,280,210,326 (approximately USD 19 million). Financing will be provided through a loan from the Development Bank of Latin America and the Caribbean (CAF), approved under Law 6897/2022. An advance payment of 10% of the contract is foreseen, and the validity will extend until the final acceptance of the works.

Bid Maintenance Guarantee Bidders are required to submit a bid maintenance guarantee equivalent to 5% of the bid amount, either through a bond or a bank guarantee.

Award System The contract will be awarded be based on the lowest economically advantageous offer, provided that it complies with the substantial conditions of the bidding documents.

Subcontracting Subcontracting is permitted; however, subcontracted works may not exceed 20% of the total contract amount.

Contracting Authority MOPC.

Relevant Dates Key dates in the process are as follows: (i) October 13, 2025, as the deadline for submitting questions;

(ii) October 17, 2025, for the submission of bids (09:00 a.m.) and their opening (09:30 a.m.) in the Assembly Hall of the MOPC Central Building.

Through this tender, the MOPC continues to advance the consolidation of Route PY21 as a strategic corridor for agricultural production, strengthening market access and contributing to the development of local communities.

IV. Executive Branch submits Bill to create the Ministry of Industry, Commerce, Tourism, Mining and Energy

On July 24, the Executive Branch submitted to the National Congress the bill entitled “To Creat the Ministry of Industry, Commerce, Tourism, Mining and Energy” (the “Bill”), which seeks to merge and reorganize various areas of the Executive into a single ministry with expanded powers over industrial, energy, mining, and tourism matters.

Institutional Framework

The Bill provides for absorbing the Ministry of Industry and Commerce, the Vice Ministry of Mines and Energy (currently under the MOPC), and the National Secretariat of Tourism. Consequently, the new ministry would be organized into 5 vice ministries: Industry; Commerce and Services; MSMEs; Tourism; and Mines and Energy.

Article 7 of the Bill sets out its functions and powers, which include formulating national policies in industrial, commercial, energy, mining, and tourism; issuing regulations and technical guidelines; and representing the State before autonomous entities in the sector.

Powers in the Energy Sector

The new ministry will assume, among others, the following responsibilities:

Formulate national energy and mining policy.

Establish technical guidelines for the management of energy and mineral resources.

Grant authorizations, permits, licenses, approvals, contracts, and concessions.

Regulate, oversee, and supervise activities related to energy, mining, and hydrocarbons.

Implement policies to ensure energy security, including the expansion of electricity generation from different sources.

These provisions would integrated into the current regulatory framework, which includes, among others, Law 966/64 (Organic Charter of ANDE) and Law 6977/22 (Promotion of Non-Conventional Renewable Energies, currently under amendment)1. If enacted as originally drafted, certain powers currently vested in ANDE under Law 966/64 would be transferred to the new ministry.

Cross-Cutting Scope

Beyond its powers in the energy sector, the ministry would be empowered to promote national industry, foster exports, regulate quality standards, encourage technological innovation, and develop policies for cultural and ecological tourism. It may also establish fees for administrative services and participate in international negotiations related to trade, energy, and mining.

Legislative Process

The Bill is currently under consideration in the Chamber of Deputies. It has already received opinions from the Committees on Economic and Financial Affairs, Budget Execution Control, Legislation and Codification, and Energy and Mining. Its discussion, originally scheduled for the plenary session on September 16, 2025, was postponed. The full text is available at the following here.

V. MOPC moves forward with public call process for the Urban Access to Route PY02 Expansion Project

In August, the MOPC held informative sessions to present the project to expand of the Urban Access to Route PY02, a strategic initiative designed to improve connectivity between Greater Asunción and cities in the country’s interior.

The project includes the construction of an elevated urban highway stretching nearly 4 kilometers, with two roadways and four lanes, connecting Ñu Guasú and Silvio Pettirossi avenues, complemented by two new access corridors to Route PY02.

The first, the so called Ypacaraí – Areguá – Luque Corridor, starting at km 41 of Route PY02 and including a new bypass in Areguá, designed to streamline traffic and boost local trade and tourism.

The second, the Ypacaraí – San Bernardino – Luque (Tarumandy) Corridor, beginning at km 43 and including lane duplication, urban improvements, and direct access to Nueva Colombia and Route PY02 itself.

The works will be executed by Rutas del Este S.A., the Route PY02 concessionaire under a Public-Private Partnership (PPP) scheme, with an estimated investment of USD 180 million. The project is currently in the public call process for competitive subcontracting of the works.

This project not only seeks to significantly reduce travel times between Greater Asunción and the country’s interior cities, but also to generate positive impacts on road safety, regional tourism, and economic competitiveness, consolidating itself as one of the most important urban interventions in Paraguay’s road infrastructure.

VI. MOPC awards the International Public Tender for the duplication of Route PY01

On September 23, the MOPC announced the award of International Public Tender No. 3101 (the “Tender”) for the improvement and duplication of Route PY01, along the 108-kilometer section between Cuatro Mojones and Quiindy (the “Project”). The Project will be executed under the Public-Private Partnership model, in accordance with Law No. 5102/13 and Regulatory Decree No. 1467/2024.

The award was granted to the consortium Rutas del Mercosur (the “Consortium”), composed of Tecnoedil S.A. (a Paraguayan company), Alya Constructora S.A. (a Brazilian company), Construpar S.A. (a Paraguayan company) and Semisa Infraestructura S.A. (an Argentine company).

The proposal submitted by the Consortium includes a Deferred Investment Payment of USD 24,077,936.70 (VAT included), which represents an 8% reduction compared to the reference value set forth by the MOPC, within a total investment project exceeding USD 400,000,000.

The initiative covers the duplication of Route PY01 from Cuatro Mojones, in the Central Department, to the city of Quiindy, in Paraguarí, spanning a total of 108 kilometers, with maintenance for 30 years.

This is the second project implemented under the Public-Private Partnership (PPP) model in the country and includes overpasses, bypasses and service roads that will enhance mobility, boost development, and reduce travel times for thousands of users. With this Project, which represents one of the most significant urban interventions in the country’s road infrastructure, Paraguay takes another step towards the modernization of its road network and strengthens its role as a logistics hub in the region.

VII. Call for bids for maintenance dredging of the Paraguay River

On September 30, 2025, the National Directorate of Public Procurement (DNCP) published National Public Tender ID No. 475451 (“Tender”), corresponding to MOPC Call No. 108/2025, convened by the Ministry of Public Works and Communications (MOPC), for the execution of maintenance dredging works on the Paraguay River along the section from the Paraná River confluence to the Apa River mouth.

The reference value of the contract amounts to ₲ 475,098,391,960 (approximately USD 63 million), with a contract term of 36 months from the notice to proceed. The bidding process is supported by a budget availability certificate issued by the Ministry of Economy and Finance.

Scope of works The Tender is divided into 3 lots, each comprising 3 main items:

Dredging of critical navigation steps (89 in total; number subject to modifications).

Supply and installation of between 36 and 50 buoys and AIS-equipped beacons per lot, including their mooring systems and full maintenance for the 36-month contract term.

Specialized maintenance and supervision services, including surveys, inspections, and technical assistance.

The works must ensure navigability for design convoys up to 290 m in length and 65 m in beam, guaranteeing a minimum draft of 3.05 m (10 feet) plus a 0.30 m under-keel safety margin.

Key dates

October 15, 2025: deadline for questions.

October 21, 2025: submission and opening of bids.

Strategic relevance

The tendered section constitutes the country’s main inland waterway. With this intervention, the MOPC seeks to ensure the continuous operability of the Paraguayan waterway, which is essential for foreign trade and regional cargo transport.

For more information on the tender, please click on the following link: ID 475451

Infrastructure Pipeline

Our team provides access to the Infrastructure Pipeline, an updated tool that offers a clear and organized overview of the most relevant projects in the sector. Available here.

Vaporizers and nicotine-free essences are included in the category of cigarettes and tobacco products subject to the Selective Consumption Tax ("ISC"), and the minimum tax rate limit for those products is increased.

General Resolution No. 35

July 24, 2025

The National Tax Revenue Directorate (“DNIT”) extended the deadlines for registration in the Registry of Persons Linked to Customs Activities (“PVAA”).

2026 National General Budget Bill

August 25, 2025

The Executive Branch submitted the draft General National Budget for 2026 ("PGN") to Congress.

Binding Consultation No. 712

August 2025

Extension of the useful life of biological assets in plantations.

Binding Consultation No. 709

July 2025

Aspects related to electronic bills of exchange.

Binding Consultation No. 694

May 2025

Tax treatment of refunds made by the parent company abroad.

Binding Consultation No. 678

April 2025

Limitation on the deductibility of self-assigned remuneration of the owner of a sole proprietorship.

August – 2025:

► Law No. 7508/2025 – Inclusion of nicotine-free vapes and essences in the category of cigarettes and tobacco products, and increase in the minimum ISC rate for those products.

The Executive Branch enacted and published Law No. 7508/2025 in the Official Gazette, establishing health measures related to Electronic Nicotine Delivery Systems (“ENDS”), Similar Non-Nicotine Delivery Systems (“SNDS”), and other similar devices, commonly referred to as vapes, vaporizers, or electronic cigarettes. These measures include a tax measure consisting of the inclusion of (1) vaping devices and (2) their vaporizable liquids, with and without nicotine, in the category of cigarettes or tobacco products taxed by the ISC, whereas previously only tobacco products used in vaping devices were taxed.

In addition, the minimum rate for vaping devices and their essences was also increased from 18% to 22%, thus restricting the Executive Branch's power to reduce the ISC rate for these goods, while keeping it intact for other products in the same category, such as cigarettes, tobacco, etc. In practice, this will not have an im y impact, as the rate for all products in this category has already been set at 22% by Decree No. 8878/2023.

What would have an immediate impact is the new ISC tax on imports of vaping devices without essences and nicotine-free essences for vaping devices, to which a 22% surcharge is immediately added. This is an issue that importers in this sector, in particular, should pay close attention to and consider in their day-to-day operations.

► General Resolution No. 35/2025 – Extension of the validity periods for registrations in the PVAA registry.

The DNIT issued General Resolution No. 35/2025, introducing adjustments to the regulations governing the authorization, renewal, and updating of PVAA. The measure complements the provisions of General Resolution No. 30/2025 regarding the validity of registrations for importers and customs brokers.

Now, registrations for regular importers, aircraft maintenance and repair companies, and duty-free shops valid as of March 1, 2025, will be extended until October 31, 2025, rather than August 31, 2025, as initially planned. Thus, the deadline for completing this procedure before these registrations expire has been extended from one to three months. For other types of PVAA, registration remains valid until May 31, 2026, with one month to complete the procedure.

An interesting feature of the new mandatory registration schedule for the PVAA registry is that the categories of "Occasional Importer" and "Diplomats" have been eliminated, which means that registrations in these categories would not be affected by the previously indicated expiration dates, although the obligation to begin the renewal process as of August 1, 2025, remains in effect.

The resolution also provides for the possibility of the General Customs Administration authorizing exceptional treatment in duly justified cases, allowing for the partial submission of requirements without interrupting essential foreign trade operations. With these modifications, the DNIT seeks to provide greater predictability to international trade actors, while ensuring the collection of taxes and the continuity of customs operations.

► The Executive Branch sent the PGN for 2026 to Congress.

On August 25, 2025, the Executive Branch presented the General National Budget for 2026 (the "PGN") to Congress, which will be reviewed for approval. Revenues are estimated at PYG 149.17 trillion (USD 20.896 billion), while the estimated fiscal deficit for fiscal year 2026 stands at 1.5% of GDP for the Central Administration, thus returning to compliance with the limits established in Law No. 5098/2016 on fiscal responsibility.

The Executive's Message adds that the tax burden would be 11.6% of GDP and tax collection would grow by 8% compared to 2025. Real GDP growth in 2026 is projected at 3.8%. No changes or eliminations of exemptions are expected, meaning that tax policy will remain stable in 2026.

The PGN bill sets limits on bonuses and prohibits gratuities, except for officials of the National Tax Revenue Directorate (DNIT). It also provides for the obligation to use the National Development Bank (BNF) for inter-institutional payments and compensation without affecting tax revenues.

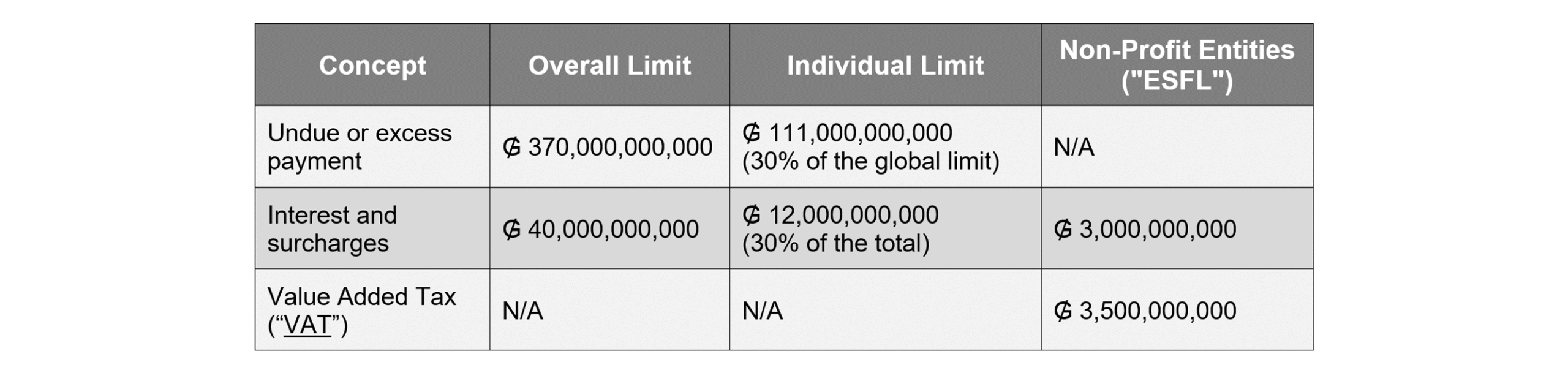

The PGN also provides for tax measures, one of which is annual budget limits for crediting taxpayers with the balances due to them for (1) undue or excess payments and (2) legal accessories. This is a budgetary measure that has been implemented every year since Law No. 5061/2013 (see Article 7) and Decree No. 850/2013. For fiscal year 2026, the PGN bill establishes the following overall and individual (per taxpayer) budget limits:

The overall limits represent the maximum amount that the DNIT can credit for the items indicated throughout the 2026 fiscal year, while the individual limits per taxpayer are 30% of the overall limit for each item. This means that no taxpayer can represent a percentage of credits greater than that indicated, thus preventing one taxpayer from excluding the others.

These budget limits do not apply to VAT refunds to ESFLs as a result of court rulings, as these have their own limits. In addition, the way in which this item is credited to ESFLs also differs from the normal regime, as these amounts are paid in cash and not credited to the taxpayer's tax account, as is the case in other instances.

If the total budget limits are reached during the fiscal year, the amounts pending credit are deferred to the following fiscal year without generating legal accessories. The area responsible for making the credits must correlatively record the resolutions that provide for them, for inclusion in the PGN for the following fiscal year.

► Binding Consultation No. 712 – Extension of the useful life of biological assets in plantations

The DNIT was consulted regarding the possibility of extending the useful life of the Neem tree plantations that make up a company's fixed assets, with the aim of starting their depreciation in 2024, extending the depreciation period to 20 years from then on, and recognizing this expense as deductible in the determination of the IRE.

In its ruling, the DNIT decided to authorize the requested extension, establishing that the plantations in question may be depreciated over a period of 20 years. It also ruled that the depreciation from these assets will be deductible for income tax purposes starting in fiscal year 2025, although, unfortunately, it did not elaborate further on the start date of the depreciation of the plantations, which, according to Article 30, paragraph 2, of the annex to Decree No. 3182/2019, is from the first harvest or cut.

The decision is based on the powers provided for in the last paragraph of Article 31 of the Annex to Decree No. 3182/2019, which allows the DNIT to set a useful life other than that specified in the regulations when supported by a technical report.

The resolution highlights that the useful life of biological assets is directly linked to the calculation of depreciation, which requires determining both the period of use and the residual value of the asset. In this case, the firm provided technical reports demonstrating that the cultivated species has a useful life of 20 years, exceeding the 5 years originally provided for in the regulations.

The DNIT specified that the authorization is limited exclusively to the assets identified in the application and is not extendable to other similar assets that have not been subject to technical analysis. Finally, it recalled that, in order to be deductible, depreciation must comply with the general requirements established in Article 14 of Law No. 6380/2019: it must be necessary to maintain the source of production, represent an actual expenditure, be properly documented, and be in line with market value.

This ruling confirms the importance of technically supporting any request to modify the useful life of depreciable or amortizable assets, especially in the case of biological assets whose productivity may vary depending on operating conditions.

► Binding Consultation No. 709 – Aspects relating to electronic bills of exchange.

In a recent binding consultation, the DNIT was asked whether it was possible to incorporate the fields provided for in Law No. 6542/2020 on bills of exchange into the electronic invoice format in order to guarantee the validity of such documents as enforceable instruments in the event of legal collection.

In addressing this issue, the DNIT distinguished between information on the exchange invoice that is validated by the Integrated National Electronic Invoicing System ("SIFEN") and information that is not, the former being either mandatory or optional. It is this validatable information that is sent to the SIFEN, as provided for in the current technical documentation. Consequently, any electronic invoice that includes bill of exchange information that differs from that provided for in the technical documentation will not be approved by the system.

The current version of the SIFEN technical documentation strictly establishes the fields that can be included, and these do not include those relating to the assigned debt, as required by Law No. 6542/2020. However, the regulations do allow space on the electronic invoice for the inclusion of additional information from the issuer (field J003, up to 5,000 characters in length), in which any other information that the issuer deems relevant may be included, such as that required by Law No. 6542/2020.

This data may appear in the electronic document or in its graphic representation (“KuDE”) sent to the customer, but it is not included in the XML file sent to SIFEN for validation, nor will it form part of the electronic tax document approved by SIFEN. In summary, taxpayers seeking to issue exchange invoices must take into account the distinctions made between validatable and non-validatable information for the purposes of including the relevant information.

► Binding Consultation No. 694 – Tax treatment of refunds made by the parent company abroad.

The DNIT issued a ruling on the tax treatment applicable to reimbursements received from its parent company in Spain. The operation consisted of the branch in Paraguay advancing certain expenses—such as hiring personnel, market studies, and technical support—which were subsequently reimbursed by the parent company under a contract called a "transitional mandate." The company understood that these amounts did not constitute taxable income and, consequently, should not be subject to VAT, Corporate Income Tax ("IRE"), or Non-Resident Income Tax ("INR").

The DNIT concluded that the reimbursements in question did not correspond to a mandate contract, but rather to the provision of services, which meant that they were subject to the local tax regime. In particular, it determined that:

The transactions must be framed within the Special Rules for the Valuation of Transactions, given the nature of related parties.

The agreed profit margin will be subject to INR, although it should have referred to IRE, since this margin would belong to the local branch.

The amounts paid by the parent company to the branch are subject to VAT, as they constitute services used in Paraguayan territory.

Payments to suppliers in Brazil will be subject to INR and VAT when the services are used or exploited in Paraguay and are linked to income taxed by the IRE.

To reach this conclusion, the DNIT examined the contract submitted, which expressly defined the relationship as a provision of services aimed at market opening, technical support, and administrative management in Paraguay and Brazil. In view of this, it considered that this was not a mere reimbursement under mandate, but rather a scheme of services provided to the foreign parent company.

The DNIT also pointed out that, as the parties were related, the transaction had to comply with the principle of independence set out in Law No. 6380/2019, so that the prices and conditions were comparable to those that would have been agreed by independent parties in similar circumstances. Finally, it insisted that the documentation must accurately reflect the concepts of "reimbursement" and the corresponding expenses in order to adequately support the accounting and settlement of taxes.

With this ruling, the DNIT sets an important precedent: reimbursements from the parent company to the local establishment, when related to the provision of services, are subject to IRE, INR, and VAT under the conditions indicated.

► Binding Consultation No. 678 – Limitation on the deductibility of self-assigned remuneration of the owner of a sole proprietorship.

The DNIT has issued a response to a binding consultation addressing the deductibility of self-assigned remuneration by the owner of a sole proprietorship, in their capacity as a taxpayer of the IRE and Personal Income Tax ("IRP"). The consultant wanted to know whether, when paying IRP on his remuneration as the owner of the sole proprietorship, this was deductible only up to 1% of gross income on the General IRE form.

The DNIT concluded that the deductibility of self-assigned remuneration in the IRE depends on the type of service provided by the owner:

100% deductibility: If the remuneration is received for independent personal services, the entire amount is deductible in the IRE. This deduction applies as long as the service provider (a) is an IRP or INR taxpayer, and (b) is not considered "senior staff" of the company.

Deductibility limited to 1% of gross income: If the remuneration is received as senior personnel, the deduction will be limited to 1% of the company's gross income for the fiscal year, regardless of whether or not the owner is an IRP taxpayer, which allows for greater flexibility than that provided for in the regulations.

In this regard, the DNIT clarified that the total deduction (100%) for independent personal services applies if the owner, partner, or shareholder, who is an IRP or INR taxpayer, receives remuneration for the provision of such services to himself in his capacity as a sole proprietor, which must be duly documented by means of a contract and a sales receipt to justify the total deductibility. In this way, the DNIT seems to be indicating that this would be possible if a person contracts with themselves for services other than those of the senior staff of the sole proprietorship.

El Ministerio de Trabajo, Empleo y Seguridad Social (MTESS) emitió la Resolución Nº 915/2025, por la cual se modifican artículos del Anexo N° 2 de la Resolución MTESS N° 991/2024, de fecha 17 de octubre de 2024, que aprueba el reglamento para la inscripción patronal en el Registro Obrero Patronal del Ministerio de Trabajo, Empleo y Seguridad Social y el reglamento para las comunicaciones establecidas en el Capítulo II del Anexo al Decreto N° 1989/2024. Esta resolución introduce cambios importantes a la Resolución Nº 991/2024 sobre la inscripción patronal y las comunicaciones en el Registro Obrero Patronal (REOP).

Principales modificaciones

Entrada de trabajadores no dependientes

La comunicación de entrada de trabajadores independientes, extranjeros temporales, tercerizados, contratistas, subcontratistas y cooperativas de trabajo asociado será voluntaria hasta que exista una regulación específica.

Se entenderá como prestación habitual aquella de al menos 16 horas semanales o 64 mensuales, durante más de 60 días.

La comunicación voluntaria deberá realizarse mediante la planilla de personal no dependiente del sistema REOP. Esta voluntariedad se mantendrá hasta que se emita un acto administrativo que regule específicamente el tema.

Salida de trabajadores no dependientes

Si la empresa optó por comunicar la entrada, la comunicación de salida será obligatoria y deberá registrarse en la planilla de personal no dependiente.

Plazo para comunicar el pago de aguinaldo

Se amplía el plazo: podrá comunicarse hasta los primeros 10 días hábiles del año siguiente al pago.

Exoneración de aranceles del costo del Certificado Laboral

Los empleadores que mantengan actualizada la planilla de personal no dependiente estarán exonerados del costo del Certificado Laboral

No aplicación de multas

Mientras rija la voluntariedad de la comunicación de entradas, no se aplicarán sanciones por comunicaciones tardías de entrada y salida de los casos citados en esta resolución.

Implicancias prácticas

Los empleadores tienen un incentivo económico (exoneración de arancel correspondiente al Certificado Laboral) para comunicar voluntariamente estos datos.

La medida introduce flexibilidad y busca una implementación gradual para las empresas.

Es fundamental actualizar procesos internos y verificar las planillas en el sistema REOP.

This content is for general informational purposes only and should not be considered as specific legal advice. If you require specific legal counsel, please do not hesitate to contact us.

Establishes a new tax incentive regime for domestic and foreign investment. This law replaces Law No. 60/1990 (the "Law 60/90"), modernizing it and incorporating new provisions.

Ley N° 7.547

September 8, 2025

Establishes the new maquila regime, which modernizes the system previously established by Law No. 1,064/1997 (the "Previous Maquila Law") and creates new provisions.

Ley N° 7.546

September 8, 2025

Creates a special regime for the production and assembly of electrical, electronic, electromechanical, and digital equipment.

The respective drafts of the three laws were submitted by the Presidency to Congress on July 24, 2025, as part of a package of regulations aimed at promoting investment in Paraguay. Both houses of Congress approved the bill, and the President signed the new laws into effect on September 9.

Development

► Law No. 7,548/2025:Establishes the new tax incentive regime for domestic and foreign investment, replacing Law 60/90.

Law No. 7,548/2025 on the "New Tax Incentive Regime for Domestic and Foreign Investment" (the "New Regime") modernizes and replaces the legal regime previously established by Law 60/90, which had been in force since 1991. This comprehensive reform is particularly relevant for domestic and foreign companies planning to invest in Paraguay, as it introduces renewed tax benefits and more agile mechanisms for accessing incentives.

According to official data contained in the explanatory memorandum of the bill, the regime established by Law 60/90 had facilitated the raising of capital for a cumulative amount, between 1989 and 2024, of more than USD 10.255 billion. In the last decade, the average annual investment reached approximately USD 329 million, of which 64% corresponded to domestic capital and 36% to foreign capital. These results are expected to improve with the New Regime, especially in Paraguay's current macroeconomic context, and this is expected to influence an increase in the national GDP.

The new regime maintains the existing key incentives but incorporates important innovations, especially the equalization between domestic and foreign investors for the exemption from the Dividend and Profit Tax (IDU). Companies that make investments exceeding USD 13,000,000 will be eligible for IDU exemptions for up to 10 years, in addition to other substantial tax benefits.

Among the main tax benefits contained in the new legislation, the following are maintained and expanded:

Exemption from customs duties and Value Added Tax (“VAT”):For the importation of capital goods intended for the production cycle. The granting of this benefit is conditional upon: (a) there being no domestic production of capital goods that are functionally compatible with those to be imported; and (b) the Paraguayan industry not supplying the goods required by the investment project in terms of quality and quantity. The determination of the availability and functional compatibility of domestic production is the responsibility of the Ministry of Industry and Commerce (MIC), which will decide on the basis of a prior non-binding technical report issued by the Paraguayan Industrial Union (UIP) or another organization deemed relevant.

Exemption from customs duties on imports: Of raw materials and inputs intended for the manufacture of capital goods established in the investment project.

VAT exemption on the first sale: Of capital goods that have been imported or purchased on the Paraguayan market under this New Regime, which have direct application in the productive or agricultural cycle. This exemption applies exclusively when the sale is made between beneficiaries of this New Regime.

Exemption from Non-Resident Income Tax (INR): On interest and commissions remitted abroad for cash loans (investments ≥ USD 13,000,000). This tax benefit applies for the duration of the project financing.

IDU Exemption: For up to 10 years for investments of ≥ USD 13,000,000, now available for both domestic and foreign capital. The granting of this benefit maintains the conditions established under Law 60/90 and applies exclusively to investors without tax residence in Paraguay, i.e.: (a) the investment must not come from a low or zero tax territory ("BONT"); and (b) in the hypothetical case that IDU withholding applies, the tax withheld is not recognized as a tax credit for the investor in their country of tax residence.

Transfer between beneficiaries: It allows the transfer of imported capital goods that have benefited from the New Regime between beneficiary companies that have biministerial resolutions, without paying the import taxes originally exempted. The asset benefiting from the New Regime must remain the property of the beneficiary entity for a minimum period of five years, counted from the date of dispatch in the case of imported goods, or from the date of acquisition for goods produced by domestic manufacturers. If the goods are transferred before the five-year period is completed, the beneficiary is obliged to pay the full amount of the taxes originally exempted.

In addition, the New Regime introduces the following additional changes:

Guarantee trust: A new mechanism for financing investment projects, which allows for the creation of a guarantee trust with capital goods benefiting from the New Regime.

Limited renewal: Benefits may be renewed within a maximum period of 20 years from the first grant, avoiding the indefinite permanence of tax incentives.

Greater control: Monitoring mechanisms are strengthened with on-site and off-site surveillance, plus random checks. The body responsible for controls will be the Executive Secretariat of the Investment Council.

For companies currently enjoying benefits under Law 60/90, these will be maintained until their expiration, in accordance with the joint ministerial resolution by which the benefits were granted. However, renewals and supplements must comply with the provisions of the New Regime. With its publication and enactment, the New Regime is now in force. The Executive Branch must issue the regulatory decree for the New Regime within 120 days of the entry into force of the regulation.

► Law No. 7,547/2025:Establishes the new maquila regime, which modernizes the legal system that had been established in the previous Maquila Law.

Law No. 7,547/2025 "On the New Maquila Regime" (the "Maquila Law") modernizes the regulatory framework of the maquila regime, which had been in force since 1997. Under the previous maquila regime, approximately 30,000 jobs were created, generating USD 1.084 billion from exports of goods and USD 32 million from exports of services by the end of 2024, according to official data.

This comprehensive reform of the maquila regime brings important changes for maquila companies, especially in terms of taxation. The main objective of the new Maquila Law is to modernize the system and make it more competitive, as well as to align the existing tax incentive regime with international recommendations on the matter.

The new Maquila Law introduces official recognition of service maquilas, fully incorporating them into the regime and extending to these activities the same benefits enjoyed by industrial maquilas. In the case of service maquiladoras, the refund will be subject to a specific limit: up to a maximum of 0.5% of the value added in the national territory or of the value of the export invoice issued by order and on behalf of the parent company, whichever is greater.

The law clarifies that the refund will not be applicable to items related to professional fees, explicitly excluding this category of services. In addition, the refund will be conditional on compliance with the requirements established in Article 12 of the law itself, related to national employment, investment, and alignment with development policies.

The text also proposes institutional changes. The National Tax Revenue Directorate will become part of the National Council of Maquiladora Export Industries (CNIME), granting greater supervisory and control powers to the Executive Secretariat. It also provides for the simplification and digitization of procedures related to the regime, with the aim of facilitating its operation.

In terms of taxation, an updated regime is consolidated. The single tax of 1% on national added value or on the export invoice is maintained, while guaranteeing the express right to a VAT tax credit refund. It also provides for the exemption from Corporate Income Tax ("IRE") on income from officially approved maquila programs, further clarifying the application of the regime. In addition, the exemption from all other Paraguayan taxes (e.g., commercial license) is maintained, with the exception of fees corresponding to services actually received. It should be noted that the owners, partners, or shareholders of maquila companies are exempt from IDU and Personal Income Tax (“IRP”) on dividends they receive from maquila companies, in accordance with the provisions of Law No. 6,380/2019, which establishes Paraguay's general tax regime.

A key point of the new Maquila Law is that it establishes a period of twenty (20) years as the maximum duration of benefits for maquila companies to operate under this regime, something that was not provided for under the previous system. The aforementioned twenty-year period is counted from the date of the administrative act approving the maquila program. During that period, the beneficiary may request a renewal of the regime for an additional period equal to the one initially granted, or up to the maximum duration, provided that it meets the requirements. This new limit is based on an alignment with best practices in fiscal policy for granting benefits, as indicated by the Organization for Economic Cooperation and Development (“OECD”), which suggests limiting the duration and renewal of tax exemptions to prevent the indefinite permanence of incentives, avoid distortions, and protect the tax base.

Finally, a transition period is provided for maquila programs currently in force under Law 1064/97. These will have a period of twelve months to comply with the new provisions of the enacted Maquila Law, with automatic incorporation into the new regime without loss of acquired rights. The protection of investments already made is also ensured, providing legal stability to companies currently operating under the scheme.

► Law No. 7,546/2025:A special regime is created for the production and assembly of electronic, electromechanical, and digital equipment.

Law No. 7,546/2025, "Establishing the National Policy for the Production and Assembly of Electrical, Electronic, Electromechanical, and Digital Equipment," seeks to diversify the Paraguayan economy through specific tax incentives for the technology sector, with the aim of significantly transforming the country's industrial landscape.

The expected impact of this new law is significant. It seeks to attract investment in technology and advanced manufacturing sectors, diversify the national productive matrix, generate skilled employment, and consolidate Paraguay as a regional technology center. Given the importance of the manufacturing sector—which currently accounts for 19.5% of GDP and employs more than 316,000 workers—the application of this regime could drive its expansion toward higher value-added activities. This new regime seeks to increase value-added activities such as the assembly of electronic, computer, and telecommunications products, which still have a marginal presence in Paraguay's manufacturing sector.

The regime offers significant tax advantages:

Exemption from customs duties on imported materials (except service fees)

Reduced VAT tax base: 15% for imports and local purchases of materials

Preferential VAT with a reduced tax base of 45% throughout the marketing circuit for products assembled under this regime

Compatibility with benefits under Law 60/90 for capital goods

Imported materials that benefited from this regime may be transferred by the beneficiary to a new investment project of the same ownership that has already been approved, subject to a favorable technical report from the Investment Council. The request must be based on: (a) definitive cessation of operations due to a duly accredited fortuitous event or force majeure; or (b) modification of the asset originally approved for assembly or production.

This regime is incompatible with any other that establishes tax deductions, exemptions, or waivers or that establishes special tax regimes. The New Tax Incentive Regime for Domestic and Foreign Capital Investment is exempt from this incompatibility.

The requirements for access to the regime are clearly defined. Interested companies must incorporate at least 20% of national added value in the production chain, generate permanent formal employment, implement technology transfer programs, and submit a complete investment project that includes, among other things, an Environmental Impact Statement.

The benefits will be granted for a period of twenty years from the date of project approval. It is possible to request renewal of the benefits of this regime for an additional period of twenty years, provided that the requirements are met again.

With its publication in the Official Gazette, this law is now in force. The Executive Branch must regulate it within 120 days.

For interested companies, it is recommended to carefully analyze investment opportunities in the electronics sector, design proposals that ensure compliance with the national added value requirement, explore strategic alliances that facilitate technology transfer, and plan large-scale projects—exceeding USD 13 million—with the support of duly registered national consulting firms.

We present a complete analysis of Paraguay’s energy regulatory framework. This publication provides a thorough overview of current legislation, the role of key institutions, licensing and contracting mechanisms, pricing structures, and investment opportunities, with a particular focus on renewable energy.

Throughout the document, we identify both regulatory barriers that may limit sector development and practical adjustments that could stimulate the market, enhance project bankability, and strengthen legal certainty. We also examine structural challenges and strategic opportunities to build a more competitive, sustainable, and diversified energy ecosystem, including the expansion of electrical infrastructure and Paraguay’s potential as a regional technology hub.

This publication is aimed at sector operators and those seeking investment opportunities, offering an up-to-date perspective that combines practical experience with strategic analysis to understand the present and future of energy in Paraguay.

For more information on any of the topics covered in this publication, please contact our experts: Manuel Acevedo (macevedo@vouga.com.py), Rodolfo Vouga Z. (rgvouga@vouga.com.py), or Yvo Salum (ysalum@vouga.com.py).

Incorporation into Paraguayan law of the new model for authorization certificates for quotas from the Southern Common Market (“Mercosur”).

Binding Consultation No. 701

June 2025

Issuance of electronic tax documents by the absorbing company with respect to invoices issued by the absorbed company, following a merger by absorption.

Binding Consultation No. 705

June 2025

Issuance of a single unnamed electronic self-invoice by financial institutions, on a monthly basis and for a lump sum, for those transactions in which the beneficiaries of payments are not required to issue invoices.

Binding Consultation No. 707

June 2025

Possibility of transferring or not transferring the remaining Value Added Tax ("VAT") credit among the members of a consortium if it is dissolved.

July 2025

Regulation

Date

Content

General Resolution N° . 32/25

22 de julio de 2025

The National Tax Revenue Directorate, (“DNIT”) regulated the procedures for applying special provisions and tax benefits for Sports Events of International Relevance (“EDRI”).

General Resolution No. 33/25

July 31, 2025

The DNIT clarified the validity of the registration of Persons Linked to Customs Activities ("PVAA") in the category of "Occasional Importer" and modified the requirements and conditions for PVAA authorization and renewal .

General Resolution No. 34/25

July 31, 2025

The DNIT modified the regulations for registration in tax identification number ("RUC"), data updates, and cancellations.

JUNE – 2025:

► Decree No. 4299/2025 - The new Mercosur quota authorization certificate model is incorporated into Paraguayan law.

Mercosur, as a regional integration bloc, has trade agreements with several countries, including Colombia and Israel. In this context, Resolution GMC No. 31/2010 was issued, approving the current "System for the Administration and Distribution of Quotas Granted to Mercosur by Third Countries or Groups of Countries" (“SACME”) in its Annex I, while approving the distribution of quotas for the Agreements with Colombia and Israel in its Annexes II and III, respectively.

In order to make the SACME operational in the day-to-day practice of international trade operators, a model certificate of authorization of Mercosur quotas was provided as Appendix I thereto, as well as a certificate of cancellation of Mercosur quotas as Appendix II. The model in Appendix I was updated by Resolution GMC No. 31/2010, incorporated into Paraguayan law by Decree No. 4299/2025.

This new model for the Mercosur quota authorization certificate introduced the flag of the issuing State Party as additional information on the document and also advanced its method of signature, which changed from handwritten to digital with authentication methods such as barcodes and QR (quick response) codes, in line with the technological advances experienced to date in international trade.

Although Resolution GMC No. 31/2010 itself stipulated that Paraguay should have incorporated it into its legal system before December 30, 2024, this was only accomplished on July 31, 2025, with the publication of Decree No. 4299/2025 in Official Gazette No. 171, at which point this process was completed.

► Binding Consultation No. 701 – Response from the DNIT on the possibility of the absorbing company issuing electronic tax documents for invoices issued by the absorbed company after a merger by absorption.

The DNIT recently clarified that, in merger by absorption processes (which could be extended to any type of merger), there is no legal impediment for the absorbing company to issue complementary documents—such as credit or debit notes—in reference to invoices previously issued by the absorbed company.

The DNIT's conclusion is based on the legal framework established by the Civil Code, which provides that, in cases of merger, the absorbing company succeeds the absorbed company in all its rights and obligations without the need for liquidation. Thus, it is also incumbent upon the acquiring company to issue tax documents reflecting refunds, discounts, rebates, or uncollectible credits related to transactions invoiced by the acquired company.

The challenge of the issue lay in the fact that both merged companies were electronic invoicers and that the Integrated National Electronic Invoicing System ("SIFEN") only allows credit and debit notes to be linked to invoices issued by the same taxpayer. To overcome this limitation, the Tax Administration confirmed that an update to SIFEN is being developed that will enable reference to the merged RUC when generating complementary electronic documents, which will be implemented through the respective technical note.

In the meantime, and in order not to interrupt the commercial operations of the electronic invoicing companies involved in the merger, the DNIT authorized a contingency mechanism: the issuance of complementary documents in physical format, provided that they are subsequently registered in the Marangatu Tax Management System ("SGTM"), in accordance with current regulations. Once the respective SIFEN update is available, companies must cancel these physical stamps and adapt to the new modality.

This clarification is key for companies involved in reorganization processes, as it ensures that tax obligations can be met without generating conflicts due to the issuance of electronic documents in the context of a merger. It also sets a precedent in the interaction between the electronic invoicing regime and the concepts of business reorganization, anticipating a technological adaptation that will facilitate future operations.

► Binding Consultation No. 705 – Response from the DNIT on the issuance of a single unnamed electronic self-invoice by financial institutions, on a monthly basis and for a lump sum, for those transactions in which the beneficiaries of payments are not required to issue invoices.

The DNIT confirmed that financial institutions will be able to issue electronic self-invoices to document transactions in which the counterparty does not issue tax receipts, such as interest payments on savings, debt securities, contributions to public entities, or certain commissions abroad. The aim is to provide legal certainty and transparency to a significant volume of transactions that, until now, lacked adequate tax support.

Financial institutions face a recurring difficulty: a large part of their expenses—for example, interest paid to savers or contributions to the Deposit Guarantee Fund—do not have invoices issued by the counterparty. This creates gaps when it comes to complying with tax reporting obligations and the Tax Administration's audit processes.

Since these items are exempt from VAT, the lack of documentation does not directly affect the collection of this tax, but it does make it difficult to trace and control expenditures in the system.

The DNIT ruled that, as purchasers, banks may issue electronic self-invoices with consolidated amounts for monthly periods, recording interest payments and other relevant disbursements, without identifying any particular counterparty in the header, since the document would cover transactions with several counterparties. These self-invoices will allow transactions to be formally documented without the need for the beneficiary to issue receipts.

Until specific regulations governing this procedure are issued within the framework of SIFEN, the monthly balance sheet reported to the Central Bank of Paraguay will be accepted as valid documentation, provided that it identifies the counterparties to the transactions, thus compensating for the lack of identification of counterparties in the monthly electronic self-invoice with consolidated amounts.

The decision is based on Law N° 6380/2019 (the "Tax Law"), which regulates the requirements for sales receipts, and Decree N° 6539/2005, which defines self-invoicing as a valid document provided that it has a tax stamp. Likewise, Decree No.° 872/2023 incorporated self-invoicing into the electronic invoicing system, specifying that it is the purchaser's responsibility to document transactions with parties that are not required to issue receipts.

The measure provides banks and financial institutions with a practical and legal mechanism to support high-volume and economically significant transactions. At the same time, it guarantees the DNIT better control over this type of transaction.

In the short term, the monthly balance sheet will continue to be valid as a supporting document, but the goal is for electronic self-invoices to become the standard tool for tax documentation of these transactions going forward.

► Binding Consultation No. 707 – DNIT response on the possibility of transferring or not transferring the remaining VAT tax credit among the members of a consortium if it is dissolved.

The DNIT clarified that, upon dissolution of a consortium, the remaining VAT tax credit cannot be transferred or distributed among its members. This balance can only be used within the consortium itself, either by offsetting it against the tax liability of the tax itself or, failing that, by computing it as a cost or expense for the determination of Corporate Income Tax ("IRE").

Consortiums formed for the execution of public works are considered independent taxpayers for VAT and IRE purposes. This means that they must keep their own accounts, issue receipts, file tax returns and, in the event of liquidation, complete a full accounting and tax closure before requesting the cancellation of their RUC.

At that stage, the consortium must settle all its tax obligations, and any remaining balance that is not used is extinguished upon dissolution. This is supported by the Tax Law, which expressly states that in no case is VAT credit refundable due to the closure or termination of the taxpayer's activity, except for exceptions provided for in the same regulation.

This means that companies that are members of a consortium in liquidation will not be able to receive a proportional share of the remaining VAT tax credit, since that right belongs exclusively to the consortium as a taxpayer.

This clarification by the DNIT provides certainty on a sensitive issue in the reorganization and liquidation of consortiums: VAT tax credits are not transferable to partners and must be absorbed in full in the accounts of the entity that is being dissolved.

JULY – 2025:

► General Resolution No. 32/25 – Regulation of procedures for the application of special provisions and tax benefits for EDRI.

Through General Resolution DNIT N° 32/25, the DNIT established the procedures and requirements for the application of tax benefits and special customs regimes for EDRI events held in Paraguay. This resolution aims to regulate the provisions of Law N° 7467/2025, which creates a legal framework to attract, promote, and regulate these events.

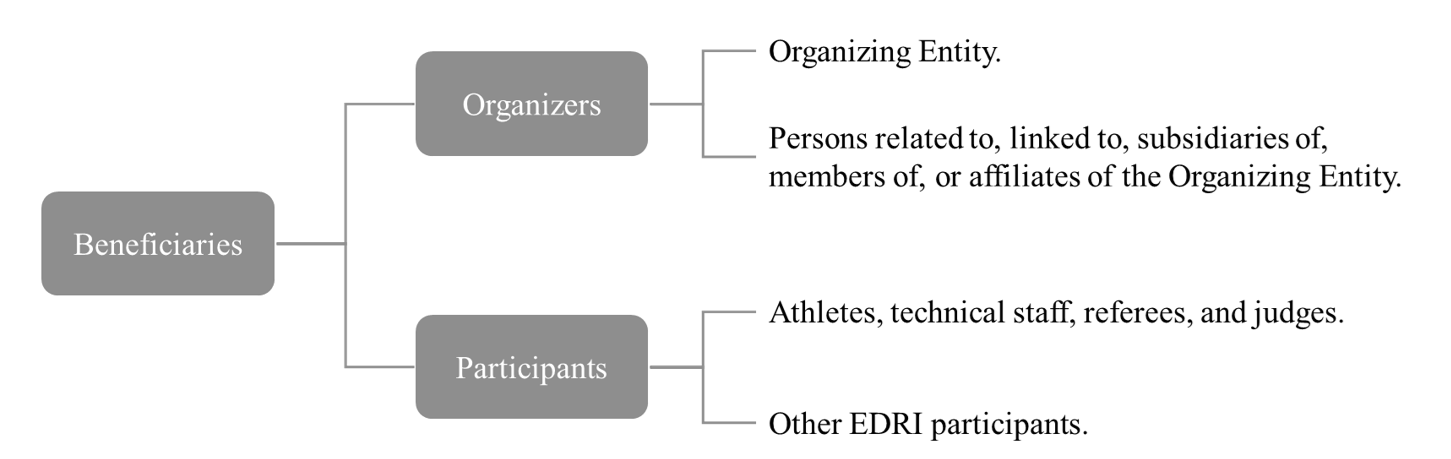

The regulation seeks to simplify procedures for "Organizing Entities" and other beneficiaries participating in events declared as EDRI by executive decree. In this regard, the resolution recognizes two groups of subjects, subdivided into four groups of beneficiaries, as follows:

The resolution specifies that exemptions from income tax and VAT on income received in connection with EDRI (including the transfer of audiovisual broadcasting and marketing rights) apply to beneficiaries of Law No. 7467/2025, provided that they are associated with EDRI in the following ways:

Organizers: Identified in the decree declaring the EDRI.

Participants: Identified in a list issued by the National Sports Secretariat ("SND").

In these cases, the decree declaring an EDRI, plus the list issued by the SND that includes the participants, where applicable, will be the documents that justify the non-withholding of taxes by local withholding agents, who must keep a copy of them in their tax files.

The regulations also authorize the entry into the country of equipment, devices, and other items related to the EDRI under the temporary admission regime, with exemption from fees, contributions, and guarantees. For the application of this regime, a detailed list of those goods must be submitted, which must be approved by the SND.

In addition to all this, the procedure to be followed to make effective the exemptions for definitive imports and donations of goods affected by EDRI is also regulated. To this end, the SND must first validate the list of goods to be imported for EDRI, or its extension, the introduction of which must be authorized by resolution of the General Customs Management ("GGA").

After that, the legal representative or authorized third party of the Organizing Entity or applicable entity may request tax clearance certificates or authorization to make the tax-free donation through the SGTM. Applicants must have an "Active" RUC and be up to date with their tax obligations, declare the official import dispatch number to the GGA, and attach the relevant documents in ".pdf" format.

The DNIT undertakes to review applications within a maximum of 20 business days. Notifications regarding the status of the application will be sent through the "Marandu" Electronic Tax Mailbox and the email address registered with the RUC.

During the analysis of applications, the DNIT may request clarifications, additional information, or documents, which will suspend the deadline for resolving applications. If the applicant does not comply with these requirements within 10 business days, the application will be considered abandoned and will be archived.

► General Resolution No. 33/25 – The DNIT clarified the validity of the registration of persons linked to customs activities ("PVAA") in the category of "Occasional Importer" and modified the requirements and conditions for the authorization and renewal of PVAA.

General Resolution DNIT No. 33/25 establishes modifications to the regulation of the PVAA registry. This new regulation clarifies the validity of the registry for the category of "Occasional Importer" and expands certain requirements for the authorization and renewal of PVAA in general.

Among the main changes, the resolution clarifies that authorization for "Occasional Importer" will be valid until December 31 of the year in which the authorization is granted, in all cases, and not only for those who do not operate in the domestic market and whose RUC is in "Canceled" status.

In addition, the documentation requirements for the PVAA registration or renewal process have been expanded:

Individuals: In all cases, they must attach a scanned copy of their identity document, including both sides (front and back), signed at the bottom of the document. The file must be in "*.pdf" format.

Legal entities: Only once, the first time they apply for authorization or renewal (whichever comes first), they must attach a scanned copy of the identity document of the principal legal representative. This document must also include both sides (front and back), be signed by the representative, and be submitted in ".pdf" format.