On Wednesday, February 22nd, 2023, the National Public Procurement Office (Dirección Nacional de Contrataciones Públicas) published on its website the call for bids “DIPE No. 01/2023 Prequalification of the Public Investment Project for the Expansion and Improvement of Route PY01 in the Cuatro Mojones-Quiindy Section” (ID 1288) (the "Project").

The call for bids for the Project is now open for the prequalification of interested bidders, who may download the bidding documents by accessing the following link. The deadline for submitting prequalification requests is May 31, 2023.

Once the prequalification of interested bidders is complete, the “competitive dialogue” (dialogo competitivo), will take place allowing prequalified bidders to make queries, suggestions and proposals to the contracting administration to clarify any issues they deem appropriate regarding the bidding documents. The competitive dialogue stage was introduced through Regulatory Decree No. 4183/2020 of PPP Law No. 5102/2013 with aims to speed up the clarification of the Project documents and where prequalified bidders will be able to address structuring and bankability issues.

The Project may adopt a repayment and financing structure similar to the those adopted for similar projects such as the expansion and improvement of Route PY02, which involve concession of the works.

The estimated value of the Project is approximately USD 566 million, according to data available in the Project Bank of the National Public Investment System (Sistema Nacional de Inversión Pública).

The Executive Branch approved the public initiative project "Expansion and Improvement of Route PY01 in the Cuatro Mojones - Quiindy section" last January 30, 2023, through Decree No. 8779/23 (the "Project"). The Project was approved under Law No. 5102/2013 on Promotion of Investment in Public Infrastructure and Expansion and Improvement of Goods and Services in Charge of the State ("PPP Law").

In accordance with the PPP Law and its Regulatory Decree No. 4183/2020, the Public Private Participation Unit (Unidad de Participación Público Privada) of the Technical Office of Planning (Secretaría Técnica de Planificación) and the Ministry of Finance (Ministerio de Hacienda) approved the feasibility of the Project and it was added to the project bank of the National Public Investment System (Sistema Nacional de Inversión Pública) ("SNIP") with SNIP code No. 973, in charge of the Ministry of Public Works and Communications (Ministerio de Obras Públicas y Comunicaciones).

The Project seeks to increase capacity of and improve traffic on Route PY01, Section 4 Mojones - Quiindy, which is 108 kilometers long. Currently, Route PY01 suffers from high traffic volumes and congestion, for which the Project proposes not only to accommodate the increase in traffic estimated for the next 30 years, but also to function as an alternative route to alleviate congestion on other roads. The Project has an estimated value of Gs. 4,140,296,573,777 (USD 566,278,813)[1] and includes works and services such as:

Earthworks, paving, drainage and complementary works;

Elaboration of an environmental management plan, road safety and traffic management;

Bridges, viaducts and specialized services;

Routine maintenance;

Acquisition of Environmental Services Certificates (Certificados de Servicios Ambientales) (issued by the Ministry of the Environment and Sustainable Development) (Ministerio del Ambiente y Desarrollo Sostenible);

Preparation of bidding terms and conditions;

Procurement of the contract management and inspection;

Project management and administration; and

Elaboration and approval of the final design.

The public tender for bidders interested in participating in the Project will be available in the next few days on the National Office of Public Procurement (Dirección Nacional de Contrataciones Públicas) website. If you require any additional information, please contact Rodolfo G. Vouga (rgvouga@vouga.com.py), Luis Marcio Torales (lmtorales@vouga.com.py), Juan Manuel Ros (jros@vouga.com.py) or your usual Vouga Abogados contact.

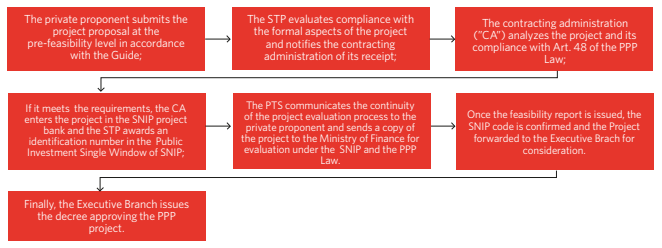

The Technical Office of Planning (Secretaría Técnica de Planificación – STP) approved through Resolution No. 277 dated December 23, 2022, the Guide for the presentation of Private Initiatives filed under Public-Private Participation regimes (the “Guide”).

The Guide is addressed to private sector participants as a reference for the presentation of private initiatives to be developed under PPP regimes, adjusted to meet requirements of the National Public Investment System (Sistema Nacional de Inversión Pública) (SNIP). The Guide, in accordance with Laws No. 5,102/2013 (“PPP Law”), No. 6,490/2020 (“Public Investment Law”), Regulatory Decrees No. 4,183/2020 of the PPP Law (the “Decree”) and No. 4,436/2020 of the Public Investment Law, was prepared with the purpose of providing a tool describing the process and requirements foreseen in the SNIP for all public investment projects, regardless of their modality and financing. Through the Guide, the STP makes available to all interested parties the procedure to file and propose private initiative PPP projects into the SNIP project bank, which was not previously established in the Decree.

The Guide includes the following information: (1) the documentation to be submitted on a mandatory basis, including any formalities involved; (2) project content requirements in the prefeasibility and feasibility stage; (3) processes subsequent to the reception by the STP; (4) prefeasibility level evaluation process; and (5) feasibility level evaluation process, including the process of issuance of the STP’s opinion of admission. In addition to the information set out above, the Guide includes a flow chart of the PPP project submission process, which is summarized below for practical purposes:

Limit for Value Added Tax ("VAT") withholding on account for local suppliers becomes effective.

September 25, 2019 (Update)

Decree No. 8612

The real estate tax values for the real estate tax and its additions, corresponding to fiscal year 2023, are fixed.

December 27, 2022

Decree No. 3108

The percentage of guarantees to be presented for the accelerated VAT refund system is fixed for 2023.

December 19, 2019 (Update)

General Resolution No. 105

The SET established the schedule of due dates for taxpayers to compulsorily adhere to the Integrated National Electronic Invoicing System ("SIFEN") - Reminder for Group 3 and following.

December 17, 2021 (Reminder)

More information:

► Law No. 6.380/2019 - Limit on VAT withholdings for local suppliers who are VAT taxpayers (UPDATE)

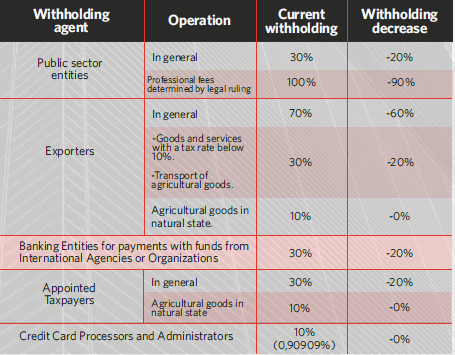

Law No. 6,380/2019 (the "Tax Law") introduced several short and medium-term novelties to the national tax regime, in respect of which its implementation is just beginning or is still pending. One of them was the limit of VAT withholdings on account, provided for in the first paragraph of Article 136. This limit was set at 10% of the tax stated in the sales receipt

The Tax Law provided for the application of such limit from the fourth year of its effectiveness, and because this provision came into effect on January 1, 2020, its implementation date was January 1, 2023. In other words, the application of this withholding limit was deferred from 2020 to 2023.

This decrease in the withholding percentage has great consequences for taxpayers that are VAT withholding agents since they must adjust their systems to the new limit. Among such taxpayers are the following:

In addition to the withholding limit, the second paragraph of article 136 of the Tax Law provided for the progressive reduction of the percentage of VAT withholdings from the year following the effective date of the Tax Law and until the deadline for applying the withholding limit is met, i.e., from 2021 to 2022.

However, this progressive reduction was conditioned to the issuance of a decree of the Executive Power providing the schedule for such purpose. Still, since this did not happen, it still needs to be complied with. Moreover, in Article 275 of Law No. 6873/2022, which approved the national budget for 2022, this reduction was suspended for that year, which, curiously, was replicated again for 2023 with Article 287 of Law No. 7050/2023, which approves the national budget for that fiscal year.

The inclusion of this suspension in the national budget law for 2023 appears as an error that may generate confusion among individuals since it refers to a rule that is no longer in force for that year because the progressive decrease was a transitory provision that could only be implemented from 2021 to 2022, but no longer in 2023, since from then on it makes sense because the withholding limit applies.

It would be appropriate for the SET to clarify the confusion that could be generated due to the suspension referred to above.

► Decree No. 8.612/2022 - The real estate tax rates for the real estate tax and its additional taxes are set for the fiscal year 2023.

Through Decree No. 8,612/2022 (the "Decree"), the Executive Branch fixed the real estate tax values established by the National Cadastre Service ("SNC") of the Ministry of Finance, which will serve as the taxable base for the determination of the real estate tax and its additions for the fiscal year 2023.

The amount of the tax is determined by applying the corresponding rates (normally 1%) on the tax valuation of the real estate established by the National Cadastre Service (taxable base), which is made up as follows:

Urban real estate: land value (m2 of the property per ₲/m2) plus building value (m2 of the buildings per ₲/m2). The ₲/m2 is determined by the type of street pavement (frontage) for the land value and the construction category for the buildings.

Rural properties: Land value (hectare ("ha") of the property per ₲/ha). The tax valuation of each district is determined according to its opportunity cost (distances to urban centers and accessibility) and the predominant type of soil according to the categories indicated in the Decree.

The tax valuation of real estate is adjusted annually according to the variation suffered by the Consumer Price Index ("CPI"), in the twelve months before November 1 of each calendar year in which such adjustment is made, as reported by the Central Bank of Paraguay. The Executive Power may make an extraordinary readjustment every five years, according to the variation in real estate value.

In that sense, the Central Bank of Paraguay informed that the variation of the CPI in the twelve months before November 1, 2022, reached 8.1%, so the Decree increased in such proportion the tax valuations for 2023. This variation can be seen for urban properties in Annex I of the Decree and rural properties in Annex II in the version of Decree No. 8736/2023.

The Decree also provides for, among other things: the valuation of properties that change from urban to rural and vice versa, the procedure for the 50% exemption for rural properties with forest priority or real right of forest surface, and the discount for rural properties with low productive areas that differ from the type of soil of their district.

► Decree No. 3,108/2019 - The percentage of guarantees to be submitted for the accelerated VAT refund regime is fixed for 2023 (UPDATE).

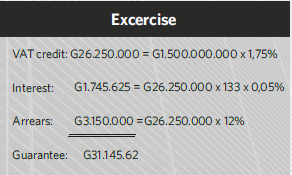

Article 102 of Law No. 6,380/2019 (the "Tax Law") provided that exporters and freight forwarders may request the accelerated refund of the VAT credit affected to their export or export freight operations by submitting for such purpose a bank guarantee, financial guarantee or insurance policy with a minimum validity of 90 business days from the date on which the refund request is submitted.

For the first three refund requests under the accelerated regime, the guarantee must cover 100% of the capital of the VAT credit required to SET, plus accessories. From the fourth request onwards, the guarantee must only cover the portion of the VAT credit resulting from the average percentage of rejected credits ("PCR") under the accelerated regime from January to November of the previous year, plus accessories.

To establish the value of the guarantee, the applicant must multiply the PCR by the VAT credit for which a refund is requested. The following legal accessories must be added to the resulting amount, calculated up to the guarantee's expiration date on the amount of the VAT credit resulting from the PCR: daily interest of 0.05% and late payment penalty of 12%.

SET publishes the PCR annually, and on this occasion published that it is 1.75% for 2023, to which it attached the following example of calculation for the guarantee:

Data

Securities

Amount requested:

₲1,500,000,000

Date of the request

05/01/2023

Warranty issued:

05/01/2023

Warranty expires:

18/05/2023

PCR:

1,75%

A more direct way of expressing the total coverage of the guarantee as a percentage of the VAT credit is achieved by expressing the accessories as percentages of the PCR. This is achieved by estimating the interest at 6.65% (133 days times 0.05%) and the late payment penalty at 12%, which, when added together, amount to 19.65% of the PCR, which can be rounded up to 20%. To add this percentage directly to the PCR, it must be expressed as 1.20 times the PCR, which for a PCR of 1.75% means a total guarantee of 2.1% of the VAT credit.

In those cases where the bank, financial or insurance policy guarantee is less than the amount rejected, the taxpayer must immediately pay the difference in favor of the Treasury, plus the legal accessories that will be calculated until the total payment.

General Resolution No. 105/2021 - The mandatory calendar for taxpayers to adhere to the SIFEN (REMINDER) was established.

All taxpayers, especially those in Group 3 of the SIFEN, are reminded that the SET issued General Resolution No. 105/2021 (the "RG"), dated December 17, 2021. Through this RG, the mandatory calendar for several groups of taxpayers to adhere to the SIFEN was established, foreseeing ten groups with nine different due dates, with a difference of one quarter between the dates foreseen for one group and another, except for groups 1 to 3, according to the following calendar.

Groups

Date from which they are obliged

1 – “Pilot plan”

July 01, 2022

2 – “Voluntary adherence”

July 01, 2022

3 – “Compulsory phase”

January 02, 2023

4 – “Compulsory phase”

April 03, 2023

5 – “Compulsory phase”

July 03, 2023

6 – “Compulsory phase”

October 02, 2023

7 – “Compulsory phase”

January 02, 2024

8 – “Compulsory phase”

April 01, 2024

9 – “Compulsory phase”

July 01, 2024

10 – “Compulsory phase”

October 01, 2024

Obligated taxpayers from groups 3 to 10 may start issuing electronically before the established date in case they wish to do so gradually. However, once the mandatory date arrives - January 2, 2023, for group 3 - they must exclusively issue all their documents electronically since the authorization and stamping of their pre-printed or self-printed documents, granted by the SET, will cease to be valid, except for the one related to virtual withholding receipts.

Taxpayers should take into account that they will bear the cost of the development and implementation of an electronic invoicing system, which often involves a considerable implementation time, as acknowledged by the SET in article 4 of the RG when it grants a period of up to 12 months of adaptation to those who wish to become voluntary electronic billers.

Therefore, it is extremely important to be aware of whether you or your company is covered by the mandatory SIFEN, because, if you are and you do not take the appropriate measures in time, you may no longer be able to operate normally. If you want to know if you or your organization are affected by this RG, you can consult the complete list of taxpayers in the complete list of taxpayers in the following search engine. For further details or better advice, don't hesitate to get in touch with our tax professionals.

The exceptional and transitory regime for the regularization of certain tax debts is extended until June 30, 2023.

December 28, 2022

Decree No. 8635

Extension until February 28, 2023, of the reduction of the VAT taxable bases applicable to the importation of goods under the tourism regime.

December 28, 2022

Decree No. 8676

The taxable base of the Selective Consumption Tax ("ISC") for the import of Gas Oil/Diesel Type III is modified until January 31, 2023.

January 03, 2023

General Resolution No. 123

The Undersecretariat of State for Taxation ("SET") establishes provisions for calculating advance payments of Corporate Income Tax ("IRE") under the general and simple regime.

December 9, 2022

More information:

Decree No. 8,634/2022 - Exceptional and transitory regime for regularizing certain tax debts is extended.

Through Decree No. 8,634/2022, the Presidency of the Republic extended the effectiveness of Decree No. 7,086/2022 (the "Decree") until June 30, 2023. The Decree was issued on May 19, 2022, and established an exceptional and transitory regime for those who regularize their tax debts to have the following benefits:

a) 0% moratorium interest rate.

b) Reduction of the fine for tax evasion up to half or up to the legal minimum, whichever is greater.

c) Payment facilities with a lower initial payment and a greater number of installments.

The tax debts eligible for this regime are those that (i) were generated in fiscal periods or fiscal years closed up to December 31, 2020, and (ii) that are in any of the following situations:

Debts consigned in the debt certificates issued by the SET that (i) have the character of firm and enforceable and (ii) are in the process of collection management by the Treasury Attorney's Office ("ABT").

Tax adjustments arising from tax assessments and application of penalties derived from audits, administrative summaries, or appeals for reconsideration which:

are pending before the courts; or

have the taxpayer's express consent or acquiescence (including those debts in collection proceedings by the SET).

Debts resulting from the filing or rectification of tax returns made by the taxpayer cannot benefit from this regime.

To access the benefit of reducing the fine for fraud, the taxpayer (i) must not have paid the penalty, even partially, and (ii) must submit a request for reliquidation, which the SET will analyze. This benefit also applies to those fines in the administrative or judicial collection.

Taxpayers wishing to avail themselves of the benefits of this regime have time to submit their request to SET or ABT until June 30, 2023, according to the new extended term. In this context, they must pay the total amount of the debt or formalize an installment plan with SET or ABT.

In case of availing of this special regime under the installment payment modality, the taxpayer must make an initial payment of at least 10% of the debt. After that, the remaining amounts of the debt may be paid in up to 36 monthly installments, on which a monthly rate of 0.75% will be applied for the term of the financing.

Exceptionally, and under the condition that the request receives the approval of the Deputy Minister of SET, the taxpayer may achieve an installment payment plan of up to 60 monthly installments if the tax debts, as a whole, exceed the amount of ₲ 1,000,000,000, without considering moratory interests.

Finally, debts originating from payment facilities that have been rendered ineffective or lapsed due to noncompliance by the taxpayer during the effectiveness of the Decree may not be financed again by the regime established therein. In addition, if the taxpayer ceases to comply with the payment facilities plan, the benefits provided in the Decree are null and void.

Decree No. 8,635/2022 - The special regime provided for in Decree No. 8,048/2022, which temporarily modifies the VAT taxable base for importing goods under the tourism regime, is extended until February 28, 2023.

To encourage border trade, the Executive Branch issued Decree No. 8,048/2022 (the "Decree"), which temporarily modified the VAT taxable base applicable to goods under the tourism regime, cited in the annex of Decree No. 1,931/2019. Through this new Decree, the validity of the previous Decree is extended until February 28, 2023.

According to the provisions of the Decree, the VAT taxable base remained at 5% for the goods referred to in the annex of Decree No. 1,931/2019. Thus, the effective rate is as follows:

Period

Taxable base

10% VAT effective tax rate

5% VAT effective tax rate

From January 1st to February 28th, 2023

5%

0,5%

0,25%

Subsequently, as of March 1, 2023, the taxable base of 15% will be applied again for importing goods under the Tourism Regime, as ordered by Article 4 of Decree No. 1,931/2019.

Decree No. 8,676/2023 - The ISC taxable base for importing Type III Diesel/Oil Gas is modified until January 31, 2023.

Through Decree No. 8,676/2023, the Executive Branch fixed, on a transitory basis, the ISC taxable base for the import of Type III Diesel/Oil Gas/Diesel, setting it at ₲3,083.3 per liter until January 31, 2023.

This decree is part of the Government's practice of temporarily fixing presumptive tax bases for Type III Diesel/Oil Gas, Virgin Naphtha, and RON 91 Naphtha, whose last iteration started on February 4, 2022, with Decree No. 6,620/2022, and concluded with December 31, 2022, with Decree No. 8,416/2022.

Thus, as of January 1, 2023, the taxable base of Virgin Naphtha and Naphtha RON 91 is determined as provided for in the ISC regulation annexed to Decree No. 3109/2019, while the taxable base of Gas Oíl/Diesel Type III is determined as provided for in Decree No. 8,676/2023, at least until January 31, 2023.

General Resolution No. 123/2022 - The SET establishes provisions for calculating the IRE advance payment under the general and simple regime.

In the last amendment to Decree No. 3,182/2019, made by Decree No. 7,402/2022, a new method for calculating IRE advances was established. Through General Resolution No. 123/2022 (the "RG"), the SET further regulated this issue.

The RG affects both IRE taxpayers under the General Regime and those under the Simple Regime, for whom the calculation of IRE advances is based on a reference amount that we will call the IRE base.

They are not obliged to pay IRE advances (i) those who have not yet closed their first fiscal year as taxpayers of this tax, nor (ii) those whose IRE base is equal to or less than ₲10,000,000.

During the taxpayer's second and third IRE taxable years, the IRE basis for the advance to be paid in the current year shall be the IRE settled in the previous taxable year before the imputation of payments on account. From the fourth fiscal year onwards, the IRE basis will be the average tax determined in the last three fiscal years before the imputation of payments on account, including the fiscal year being declared. Thus, in the declaration of xx2, the average of xx0, xx1, and xx2 must be taken for the advance payments to be paid in xx3.

The basis for calculating the advance payments will be determined by subtracting from the IRE-base the following items, in order: (i) the withholdings and deductions that were made to the taxpayer in the year declared (xx2), according to its tax return; and (ii) the balance in favor of the taxpayer in the liquidation of the IRE corresponding to the year declared (xx2), which, on certain occasions, could benefit the taxpayer with the duplication of the deduction of withholdings and deductions.

The RG foresees that when the taxpayer's credit balance for the year declared is deducted from the amount of the advances to be paid for the following tax year, this balance is reduced by the amount used against the advances, which, if so, could imply a misappropriation of the taxpayer's credit, since a credit would be offset against another credit (advance payment), instead of against a debit (tax).

If a taxpayer did not file its liquidation in any of the three years to be used for the IRE-base or if its liquidation did not show any tax payable, then the number "0" will be used for those years to perform the relevant calculations. This can be seen in the numerical example of the RG transcribed below:

Concept

Amount

Tax assessed for fiscal year xx2 Tax assessed for fiscal year xx1 Tax assessed for fiscal year xx0

180.000.000 120.000.000 0

Average income tax paid in the last 3 fiscal years (xx2 + xx1 + xx0) / 3 (180.000.000 + 120.000.000 + 0) / 3

100.000.000

Minus: withholdings and perceptions for the year xx2

20.000.000

A) Advance to be paid for the following fiscal year (xx3)

80.000.000

B) Minus: balance in favor of the taxpayer for fiscal year xx2

2.000.000

C) Basis for calculating advance installments

78.000.000

The installment of each advance payment is determined by multiplying the calculation basis for the advance payment installments ("C" in the table above) by 25% or, in other words, by dividing it by 4:

78.000.000 / 4 = 19.500.000

Each installment must be paid by taxpayers in the first, third, fifth, and seventh month after the due date for filing the tax return, according to the perpetual calendar of General Resolution No. 38/2020, which is for those taxpayers with closing on December 31 and due date of the IRE in April means in May, July, September, and November.

If from the income tax liquidation corresponding to the last fiscal year, it appears that the taxpayer has a balance in its favor ("B" in the table above) that is equal or higher than the amount of the advances to be paid ("A" in the table above), the installment of the advance payment will be equal to "0".

If the taxpayer rectifies the IRE affidavits affecting any of the elements for the determination of the advance payments or files affidavits for previous tax years that were pending, the determination of the advance payments will be recalculated, and the values will be updated in the standardized affidavit and, consequently, in the taxpayer's current tax account.

Finally, the RG approved the use of new versions of forms 500 (v3) and 501 (v2) of the IRE General and Simple Regime, respectively.

These forms will be available from January 1, 2023. They will be used for liquidating the tax corresponding to the fiscal year 2022 and for determining the advance payments for the fiscal year 2023 for those taxpayers with closing on December 31. For taxpayers that close their fiscal year in April or June, the new versions of the forms will be used for the respective 2023 closings and to determine the advance payment of their fiscal year closing in 2024.

Desde Vouga Abogados asistimos a CAF – Banco de Desarrollo de América Latina, en el otorgamiento a favor del Sudameris Bank de una línea de crédito revolvente y no comprometida por hasta la suma de USD 20.000.000.

Los fondos obtenidos por Sudameris Bank serán utilizados para financiar a sus clientes calificados como pequeñas y medianas empresas, que desarrollen sus actividades en sectores productivos de la economía nacional y en especial a aquellos que necesiten financiar operaciones de comercio exterior, capital de trabajo, inversiones en maquinaria y equipos, en eficiencia energética y negocios verdes, y las actividades económicas conexas a la industria del agro.

Entre otros, el rol de Vouga incluyó el asesoramiento a CAF durante la negociación del contrato de línea de crédito con la entidad financiera, así como la asistencia en la redacción de los documentos del financiamiento, en la debida diligencia al banco y el desembolso del préstamo.

El asesoramiento de Vouga fue liderado por el socio Carlos Vouga y el equipo conformado por el asociado senior Georg Birbaumer y los asociados Juan Manuel Ros, Paula Lovera y la paralegal Teresa Sosa.

For further information regarding this transaction or other topics related to Banking & Finance, please feel free to contact Carlos Vouga (cvouga@vouga.com.py) o Georg Birbaumer (gbirbaumer@vouga.com.py).

On September 8, 2022, the Executive issued the Decree No. 7774/2022 (the “Decree”) that regulates articles 53, 54 and 60 of Law No. 422/1973 (the “Forestry Law”), specifically with regard to offences and penalties.

The Forestry Law includes a list of offences and penalties (§§ 53-54), and some basic application rules, such as the five-year statute of limitation period, the enforcement authority, the need for summary proceedings (art. 56/59 -60). The Decree seeks to provide greater detail to allow the application of the regime of offences and penalties by the enforcement authority, the National Forestry Institute (the "Infona").

Regarding the offence’s regime, the Decree classifies them as very minor, minor, medium, serious and very serious (§ 3), and then incorporate an extensive table with seventeen typified conducts (§ 6), including the six specific infractions already foreseen in the Forest Law. As can be seen from said table, the same type of offences can be classified with different degrees depending on the case, including offences varying between very minor and very serious.

To rate offences, the Decree incorporates two "assessment methods", depending on whether or not there is a change in land use, fires or land clearing (§ 7):

(i) If yes, the first step is to set the base amount of the fine according to the number of affected hectares, at a rate of ten wages per hectare in the Región Occidental and twenty wages per hectare in the Región Oriental. Then, the mitigating and aggravating factors that may or may not take place are weighed; such as the severity of the damage caused, possibility of recovery, existence of an approved plan, collaboration with the investigation and recidivism (five years from the last firm penalty).

(ii) If there is no land clearing, it starts from a very minor penalty to reach then a final assessment after considering these indicators: damage to the legal order, intentionality, accumulation of offences within the succession of illegal conducts, recidivism, and the value of the resulting forest products and by-products.

Turning to the penalty regime, the Decree implies that Infona will apply fines in all cases, varying the amount of the fine according to the degree of the infraction. Ascending up to 10,000 minimum wages (currently PYG 980,890,000) (§ 5), in line with the cap set by the Infona’s organic charter (Law 3464/2008, § 9(s)). According to the Decree, Infona may additionally apply the other types of penalties set forth in the Forestry Law, depending on the nature of the infraction. Such penalties are confiscation, suspension of permits and disqualification for activities for up to five years, all of which are also provided for as "actions" in the Decree (§§ 4/6).

Regardless of the penalty imposed, the Decree states that the offender must rebuild the protected forests and mandatory minimum forestry reserves affected by the illegal conduct (§ 6 in fine). in fine).

Finally, the Decree provides for some acts that are not penalised, including illegal acts by third parties that are duly reported to the authorities and changes in land use aimed at fighting fires appropriately.

The Decree replaces another relatively recent regulation of 2020, reflecting the Executive's interest in improving the application of penalties for violations of forestry regulations. Like any punitive regulation, it will eventually be subject to legality scrutiny by the courts.

Article prepared for The Legal Industry Reviews, Edition N° 2, Paraguay, by Rodrigo Fernández, you can consult the complete review here.

El Directorio del Banco Central del Paraguay (el “BCP”), a través de Resolución Nro. 7 de Acta Nro. 68 de fecha 25 de noviembre de 2022 (la “Resolución”), aprobó el reglamento que establece el procedimiento y las condiciones mínimas para realizar remesas físicas de divisas al exterior. La Resolución dispone que luego de que la Superintendencia de Bancos verifique que se cumplan las condiciones mínimas y del procedimiento reglamentario, las entidades bancarias y cambiarias podrán realizar operaciones de remesas físicas de divisas al exterior.

Para poder realizar remesas físicas de divisas al exterior, por cualquier medio ya sea terrestre, fluvial o aéreo, la Superintendencia de Bancos otorgará una autorización de carácter general para operar con una determinada entidad contraparte y/o corresponsal extranjero, quién se encargará de la liquidación y pago del contravalor en cuenta bancaria.

A fin de obtener la autorización, las entidades bancarias y cambiarias, deberán cumplir con las siguientes condiciones mínimas y presentar los siguientes recaudos ante la Superintendencia de Bancos:

Identificar a las entidades corresponsales y/o contrapartes extranjeras en las operaciones de remesas físicas de divisas.

Especificar los países y las ciudades en los que estén domiciliadas las entidades extranjeras.

Presentar las constancias que acrediten que tanto la entidad contraparte del exterior, como también el corresponsal responsable de la liquidación de las operaciones, se encuentran debidamente autorizados, por el órgano de supervisión del país en los que operan, para realizar este tipo de operaciones.

Las entidades corresponsales y/o las contrapartes extranjeras deben estar sujetas a una supervisión similar a la local o a satisfacción de la Superintendencia de Bancos del Banco Central del Paraguay.

Proforma del contrato a ser utilizado entre las partes en donde se establezcan como mínimo las obligaciones mutuas de las partes y las condiciones de la prestación del servicio, entre otros.

Otros datos y/o documentaciones adicionales requeridos por la Superintendencia, en el proceso de evaluación para brindar la autorización particular, o con posterioridad.

La Resolución también establece como condición mínima que las entidades bancarias y cambiarias acrediten que tanto su contraparte extranjera como la entidad responsable de la liquidación de las operaciones, cuenten con políticas y procedimiento adecuados para la prevención del lavado de dinero, financiamiento del terrorismo y proliferación de armas de destrucción masiva.

Es de suma importancia mencionar que los países donde se encuentren domiciliadas las entidades extranjeras deben pertenecer al Grupo de Acción Financiera Internacional (GAFI) u otro organismo similar. El BCP podrá formalizar convenios de cooperación con el órgano supervisor de dichos países, de manera a compartir información en forma reciproca sobre estas operaciones.

El pasado 14 de noviembre de 2022, nuestro equipo tuvo el honor de participar en el lanzamiento de la Asociación Paraguaya de Venture Capital (PARCAPY), que reunió a importantes personalidades del sector emprendedor en nuestro país, tanto autoridades como miembros fundadores y afiliados.

Estamos muy orgullosos de ser afiliados y de apoyar desde el inicio a esta organización que tiene como finalidad la promoción y el desarrollo del capital de riesgo en Paraguay.

Desde VOUGA Abogados aportamos nuestra experiencia y nos esforzamos por ofrecer soluciones versátiles, creativas e innovadoras para el ecosistema emprendedor, tecnológico y de venture capital.

Estamos orgullosos de haber creado el primer departamento especializado en Venture Capital (Vouga VCA) de Paraguay. Nuestro objetivo es permanecer a la vanguardia en la prestación de servicios jurídicos del área para inversores nacionales e internacionales, así como también a emprendedores y startups.